Foreign direct investors often outsource “parts of compliance” (tax, payroll, e-invoicing, HR administration, data privacy, corporate secretarial) to multiple specialists. The operational logic seems sound—until something breaks. At that moment, third-party vendor risk becomes less about vendor competence and more about who owns the outcome across handovers, datasets, and overlapping obligations.

The uncomfortable truth: regulators don’t care about your vendor map

In Vietnam, the legal and enforcement framing is structurally simple: the enterprise is the accountable unit. A vendor may prepare, process, or submit on your behalf—but statutory obligations (and most enforcement actions) are evaluated against the company’s compliance posture, timeliness, and evidence.

Tax deadlines are enterprise-level obligations, even when the work is outsourced. Vietnam’s tax administration law sets clear filing deadlines for monthly and quarterly declarations (e.g., “no later than the 20th day” of the following month for monthly filings; “no later than the last day of the first month” of the following quarter for quarterly filings). These deadlines do not shift because your VAT return was “with the accounting vendor,” while your e-invoicing was “with the e-invoice provider.”

The e-invoice regime is a compliance system, not a software choice. Vietnam has a detailed legal framework governing invoices and records (e.g., Decree 123/2020), later updated by amendments such as Decree 70/2025 and implementing guidance such as Circular 32/2025 (effective from 1 June 2025, replacing earlier guidance like Circular 78/2021). If your invoicing data pipeline fails because two vendors assume the other is maintaining master data or authorization logic, the regulatory exposure still sits with the enterprise that issued (or failed to issue) compliant invoices.

Penalties attach to the taxpayer/employer, not the vendor. Vietnam’s administrative penalty framework for tax/invoice violations sets maximum fines (e.g., commonly cited caps for invoice violations and tax procedure violations for organizations). While the details differ by violation type and circumstances, the operational takeaway for FDIs is consistent: if a filing is late, inconsistent, or unsupported, the enterprise bears the enforcement cycle—requests for explanation, corrective filings, penalties, and potential downstream friction.

Payroll and social insurance are enforced as employer obligations. Administrative sanctions in labor and social insurance sit in a separate enforcement lane (not “tax”), and Vietnam’s sanctioning framework expressly covers labor and social insurance violations. If payroll is outsourced, but an insurance registration is late or contributions are misapplied, the enforcement impact is still against the employer entity.

Vietnam’s 2026 PDPL framework explicitly recognizes “third parties,” but accountability remains anchored to the core roles. The Law on Personal Data Protection (effective 1 Jan 2026) defines the ecosystem—data controller, data processor, controller-and-processor, and “third party” (bên thứ ba). A vendor can be a processor or third party depending on the operational setup, but the law’s structure still expects the responsible parties to govern processing, document decisions, and manage risks.

Crucially for FDIs, the PDPL makes cross-border data transfer governance an operational requirement: it describes cross-border transfer cases and requires an impact-assessment dossier to be prepared and submitted within a defined window (e.g., within 60 days from the first cross-border transfer, subject to the law’s conditions/exceptions). If your HRIS, CRM, or payroll platform is hosted offshore by a third-party vendor, “we thought the vendor handled it” is not a defense-grade control.

Read Related: Beyond Market Entry: The Hidden Risks of Setup-Only Market Entry Services

What the “accountability gap” looks like in real life

The accountability gap is rarely “nobody did anything.” More often, it is: everyone did their piece—and the system still failed.

Below are Vietnam-specific patterns that commonly convert multi-vendor setups into third-party vendor risk.

E-invoice vs VAT reporting mismatch – Vendor A (e-invoice service provider) controls issuance/formatting workflows; Vendor B (accountant) prepares VAT declarations based on monthly bookkeeping.

– A small master-data error (tax code format, buyer info logic, timing of issuance, or invoice correction workflow after Decree 70/Circular 32 updates) results in inconsistent records.

– Outcome: the enterprise must reconcile, correct issuance, explain anomalies, and manage penalty exposure under the tax/invoice enforcement framework.

Payroll “runs” but PIT and accounting don’t tie out – Vendor C runs payroll; Vendor D handles tax declarations; Vendor E posts costs into the general ledger.

– Benefits-in-kind, deductions, or contract changes are reflected in payroll but not consistently captured across PIT and the accounting treatment.

– Outcome: year-end settlement pressure, rework, and an audit story that is harder to defend because the evidence trail is fragmented across vendors and email threads—despite clear enterprise filing deadlines.

Social insurance onboarding falls into the “between scopes” gap – A new hire starts quickly in Ho Chi Minh City or Hanoi; the labor contract exists, but onboarding artifacts live with HR, payroll data lives with the payroll vendor, and the SI registration step is treated as “someone else’s job.”

– Vietnam’s social insurance portals and local guidance commonly emphasize a short onboarding window (often communicated as “within 30 days” from labor contract conclusion) and Decree 12/2022 provides the penalty framework for labor/social insurance administrative violations.

– Outcome: back-and-forth with the social insurance authority, corrective submissions, and avoidable enforcement exposure—borne by the employer.

PDPL cross-border transfer obligations get missed because “IT is outsourced” – The FDI uses a global HRIS or CRM hosted outside Vietnam by a third-party vendor.

– Under the PDPL, cross-border transfer cases are explicitly defined, and the law requires an impact-assessment dossier submission within a defined period (e.g., 60 days from first transfer), depending on the case.

– Outcome: the legal duty to build the dossier, document roles (controller/processor/third party), and maintain governance sits with the enterprise and its responsible roles—not with the vendor’s generic privacy policy.

Read Related: Beyond Market Entry: Managing Multiple Vendors and the Hidden Compliance Gaps for FDIs in Vietnam | InCorp Vietnam

Why multi-vendor responsibility breaks down structurally

Multi-vendor models fail for predictable reasons. They are not “bad” by default—but they are fragile in Vietnam’s compliance environment because obligations are cross-functional, procedural, and evidence-based.

Compliance is cross-functional; vendor scopes are siloed.

Vietnam’s deadlines are simple on paper but unforgiving in operations. Tax filing timelines are statutory, and tax reporting is increasingly system-driven (e-invoices, eTax). When payroll, accounting, invoicing, and HR administration are split, the enterprise must build the integration layer—or accept “between scopes” failures as inevitable.

Enforcement regimes are multiple—and they don’t coordinate around your org chart.

Tax/invoice penalties are governed under one enforcement framework (e.g., Decree 125/2020). Labor and social insurance enforcement sits in another (e.g., Decree 12/2022). Data protection now has a full law (PDPL) and an implementing decree (Decree 356/2025), effective from 1 Jan 2026. Each regime has different documentation expectations, authorities, and enforcement triggers—while the enterprise is the consistent accountable party.

The PDPL makes third-party roles explicit—and increases the cost of “unclear ownership.”

The PDPL defines “third party” and the controller/processor role logic; it also creates explicit governance demands around sensitive personal data and cross-border transfer. For cross-border transfer, the law sets a dossier requirement and a timeline (e.g., submit within 60 days from the first transfer in qualifying cases). If you use third-party vendors for payroll, HRIS, recruitment platforms, customer databases, marketing tools, or outsourced “DPO-as-a-service,” the control question is no longer theoretical—it is documentable and time-bound.

Decree 356’s forms and guidance operationalize this: they contemplate documenting the responsible PDP personnel and even the use of personal data protection service providers under contract—another indicator that vendor governance is becoming a regulated expectation, not a “nice to have.”

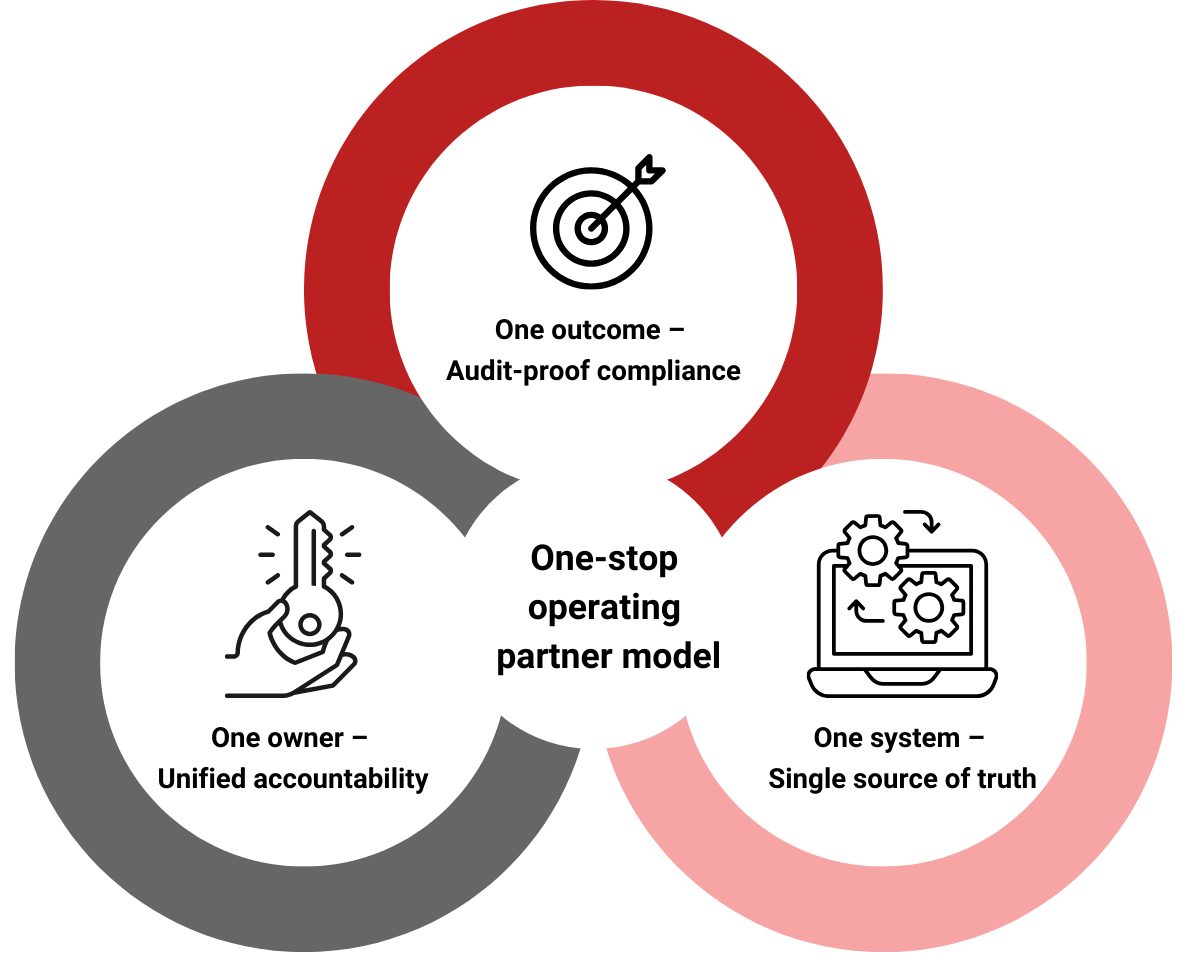

The one-stop operating partner model: one owner, one system, one outcome

A one-stop operating partner model is fundamentally misunderstood if viewed merely as “bundled administrative services.” It is, in reality, a comprehensive operating system purposefully designed to eliminate the most critical failure mode in third-party vendor management: the accountability gap.

When growing an enterprise, relying on a fragmented map of siloed vendors (one for tax, another for payroll, a third for legal secretarial) inevitably creates blind spots. The one-stop model replaces this fragmentation with an integrated architecture built on three uncompromising design principles:

One Outcome (Audit-Proof Compliance): The ultimate deliverable is not just a filed document, but a consistent, holistic compliance posture. The outcome is timely, error-free filings backed by centralized, structured evidence that can withstand immediate regulatory scrutiny

One Owner (Unified Orchestration): It replaces the classic “vendor finger-pointing” with a single point of accountability. You are no longer managing tasks across multiple agencies; you are managing a single partner accountable for end-to-end deadlines and strategic outputs. If a discrepancy arises, there is no ambiguity about whose responsibility it is to resolve it.

One System (Single Source of Truth): Compliance is deeply interconnected. A change in a foreign employee’s work permit (Legal) instantly impacts payroll calculations (HR) and personal income tax declarations (Tax). A one-stop model utilizes a shared, cross-functional dataset. This ensures that tax, payroll, invoicing, corporate secretarial, and—increasingly critical—data privacy governance (PDPL) are perfectly synchronized.

This aligns with how Vietnam’s enforcement regimes behave: they evaluate the enterprise’s compliance posture, not the vendor map.

| Dimension | Multi-vendor model (typical) | One-stop operating partner model |

| Accountability | Many task owners; unclear outcome owner (“not in scope”) | Single accountable operating owner for calendar + deliverables |

| Data | Multiple datasets; reconciliation is optional or late | One integrated dataset; reconciliation is built into the operating cycle |

| Speed | Sequential bottlenecks at handovers | Parallel execution within one coordinated team |

| Enforcement readiness | Evidence scattered; respond reactively to authority queries | Evidence centralized; structured response process |

| PDPL readiness | Vendor roles unclear; cross-border transfer governance easy to miss | Vendor roles mapped; dossiers and documentation workflows integrated |

If your Vietnam operations currently rely on multiple vendors, InCorp Vietnam can help you map third-party vendor risk across tax, payroll, e-invoicing, PDPL, then consolidate execution into one accountable operating framework—so management can focus on growth while compliance stays controlled

Learn the Right Setup for Business

Expansion in the Vietnam

Frequently Asked Questions

What is third-party vendor risk?

- Third-party vendor risk is the risk that outsourced vendors may cause compliance, operational, or data issues—but the enterprise remains accountable.

Does outsourcing reduce third-party vendor risk?

- No. Outsourcing can improve efficiency, but third-party vendor risk remains. If a vendor fails, the company still faces regulatory and financial consequences.

What is the biggest third-party vendor risk?

- The biggest third-party vendor risk is lack of coordination between vendors, leading to data gaps, errors, and missed compliance deadlines.

How to manage third-party vendor risk?

- Manage third-party vendor risk with clear ownership, centralized data, regular reconciliations, and ongoing monitoring of vendor performance.