Vietnam seafood export performance has entered a new phase of growth and structural transformation. After facing global demand slowdowns in 2023, the industry rebounded strongly in 2024 and reached a historic milestone in 2025. Today, Vietnam remains one of the world’s largest seafood exporters, supplying more than 170 markets worldwide and maintaining its position among the top three seafood exporting countries globally.

However, the competitive dynamics of the sector are evolving rapidly. Price competitiveness alone is no longer enough. Instead, the next stage of growth in Vietnam seafood exports depends on traceability, compliance with global standards, value-added processing, and diversified export markets.

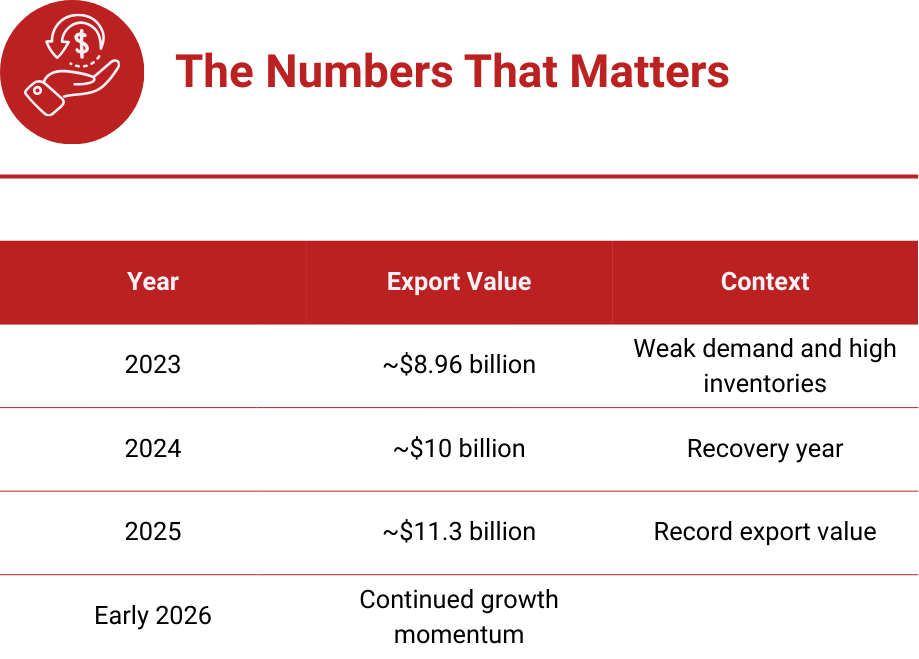

Vietnam Seafood Export Performance: 2023–2026

The last three years show how the industry has recovered from global disruptions and adapted to changing trade conditions.

According to the Vietnam Association of Seafood Exporters and Producers (VASEP), seafood exports reached approximately $11.3 billion in 2025, representing a year-on-year increase of around 13 percent.

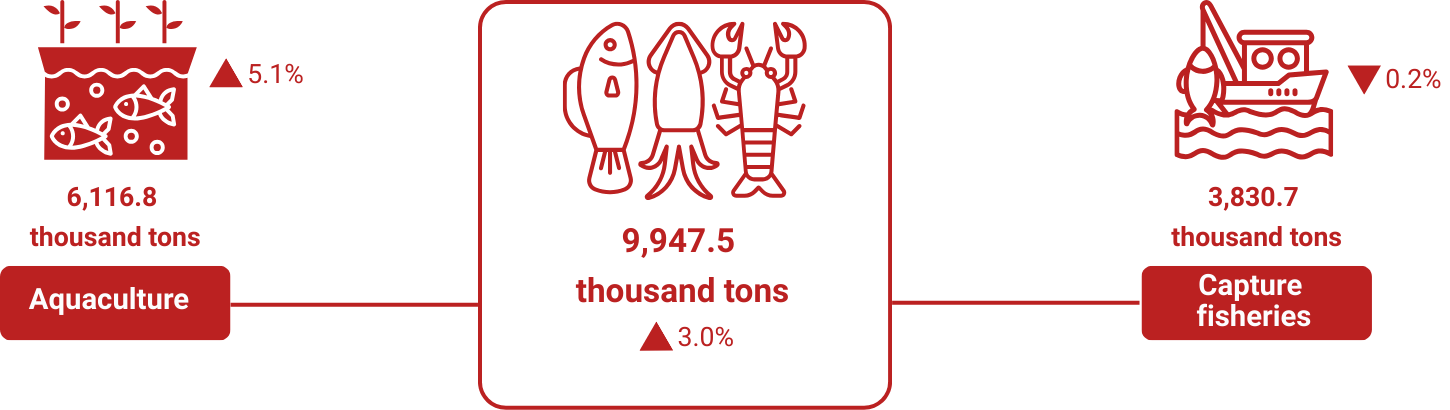

Total fisheries output is estimated at 9,947.5 thousand tons, representing a 3.0% increase compared to 2024. Fish continued to account for the largest share of production, reaching 6,962.4 thousand tons, up 2.7% year on year. Shrimp production recorded the strongest growth, rising 5.5% to 1,522.2 thousand tons, reflecting steady expansion in aquaculture activities. Meanwhile, other aquatic products reached 1,462.9 thousand tons, increasing 1.9% compared to the previous year. Overall, the growth in fisheries output was primarily supported by continued improvements in aquaculture productivity, which helped offset the relatively stable performance of capture fisheries.

This record performance reflects stronger global demand, improved production capacity, and better positioning in Asian markets. The industry has gradually shifted from purely volume-driven growth toward higher value products and diversified market strategies.

Expanding your seafood operations in Vietnam? Work with InCorp Vietnam for market entry, accounting, and regulatory compliance support across the seafood value chain.

2. Product Breakdown: The Four Pillars of Vietnam Seafood Exports

Vietnam seafood exports are built on four core product groups: shrimp, pangasius, tuna, and cephalopods (squid and octopus). Together, these categories account for the majority of the country’s seafood export revenue and shape the overall performance of the industry

These product categories are not just large in volume. Each reflects a different structural trend shaping the future of Vietnam seafood exports.

What the Product Data Actually Means

Shrimp: The Premium Shift

Shrimp remains the largest pillar of Vietnam seafood exports. In 2025, shrimp exports reached $4.6 billion, accounting for roughly 40% of the country’s total seafood export value.

However, the key shift is not only growth but changing market structure. China and Hong Kong have emerged as major buyers of premium shrimp products, while CPTPP markets such as Japan and Canada continue to provide stable demand supported by tariff advantages. At the same time, exports to the United States face greater uncertainty due to anti-dumping pressure and stricter compliance requirements.

Key insight: Vietnam’s shrimp industry is gradually moving from commodity exports toward premium segmentation, deeper processing, and stronger compliance standards.

Pangasius: The Diversification Success Story

Pangasius remains the second-largest contributor to Vietnam seafood exports, reaching approximately $2.2 billion in 2025.

Frozen fillets under HS code 0304 still dominate the product mix, generating around $1.8 billion in exports. Meanwhile, processed pangasius products remain relatively small despite offering higher margins.

Export diversification has also accelerated, with stronger growth in markets such as Brazil, CPTPP countries, and ASEAN economies.

Key insight: The next growth driver is value-added pangasius products, not simply expanding frozen fillet exports.

Tuna: The Regulatory Canary

Tuna exports reached approximately $924 million in 2025, but the sector continues to face significant challenges from supply constraints and regulatory pressure.

In particular, compliance with international regulations such as the U.S. Marine Mammal Protection Act (MMPA) is becoming a key barrier for exporters targeting the American market.

Key insight: Tuna highlights how regulatory scrutiny is increasing for wild-caught seafood, making traceability and sustainability compliance essential.

Cephalopods: The Unsung Performer

Squid and octopus exports reached approximately $759 million in 2025, making cephalopods one of the fastest-growing segments within Vietnam seafood exports.

Demand is particularly strong in Northeast Asian markets such as Japan and South Korea, where these products are widely used in retail and food service.

Key insight: Maintaining strict product specifications for mature markets while expanding semi-processed formats for emerging markets will support continued growth.

Strategic Insight for Vietnam Seafood Exports

These four product pillars reveal a broader transformation across the industry. Vietnam seafood exports are no longer driven solely by production volume. Instead, competitiveness increasingly depends on:

- premium product segmentation

- value-added processing

- diversified export markets

- stronger compliance and traceability systems

Exporters that align with these trends will be better positioned to capture growth opportunities in the evolving global seafood market.

Operating in the Vietnam seafood export sector? Partner with InCorp Vietnam for tax, compliance, and corporate solutions to keep your seafood business export-ready.

3. Destination Markets: Where the Growth Actually Is

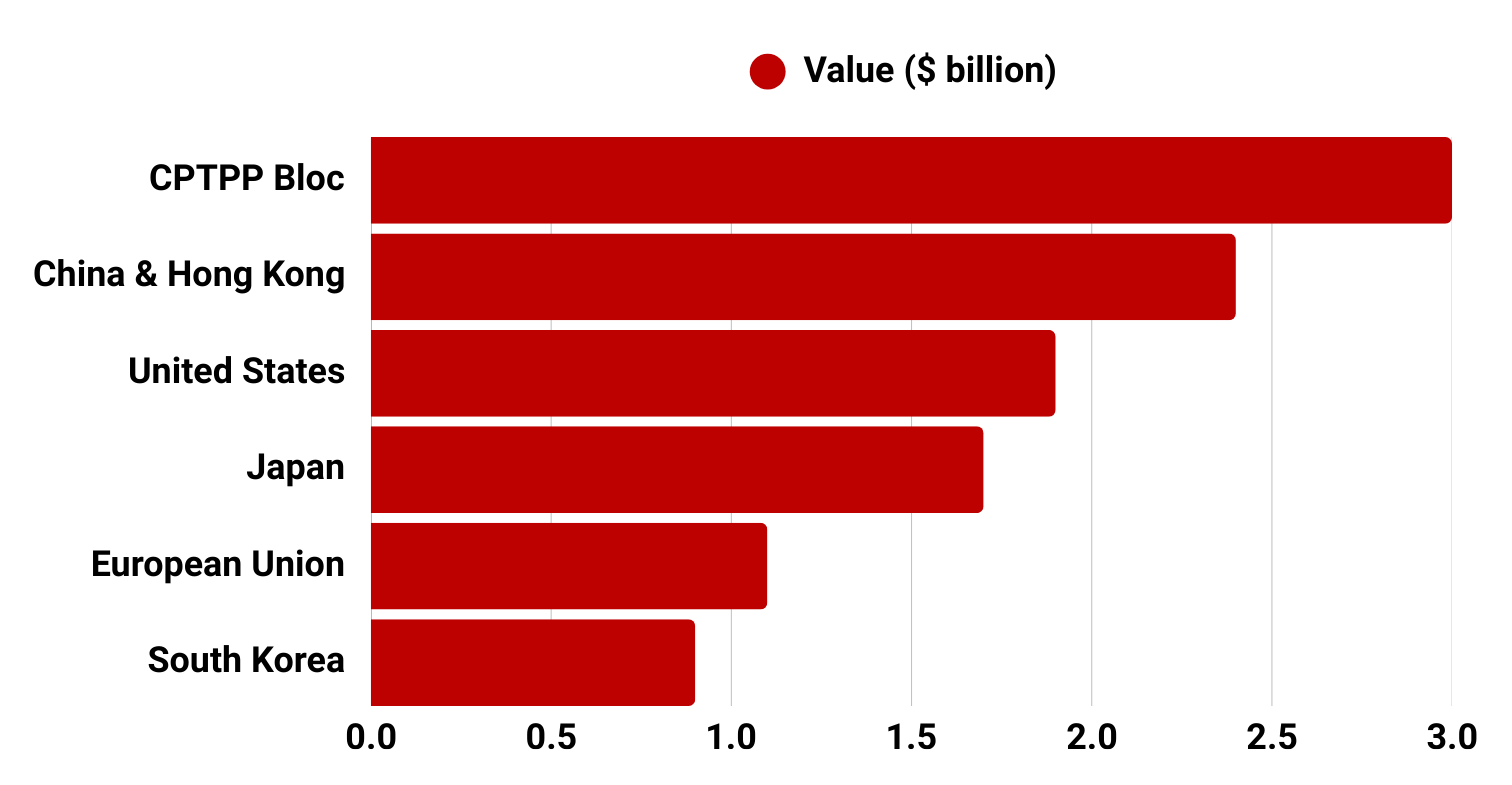

Vietnam’s seafood export structure shows a clear shift toward diversified markets and stronger regional demand, particularly in Asia and CPTPP economies.

The CPTPP bloc remained the largest market cluster, generating around $3 billion in seafood exports in 2025, an increase of about 20.8% year-on-year. Key destinations such as Japan, Canada, and Australia continue to provide stable demand thanks to tariff advantages under the trade agreement.

When viewed by individual markets, China and Hong Kong emerged as the largest single destination, reaching approximately $2.4 billion in export value in 2025, up 28.5% year-on-year. The strong growth was driven by rising demand for premium seafood products such as lobster, crab, and high-end shrimp, particularly during peak consumption periods in the Chinese market.

The United States remained a major high-value market, with imports of Vietnamese seafood reaching around $1.9 billion, although growth was relatively modest compared with Asia due to regulatory pressures, tariff risks, and stricter compliance requirements.

Meanwhile, Japan continued to be one of the most stable markets, importing roughly $1.7 billion worth of seafood from Vietnam, reflecting consistent demand for high-quality processed products and strong trade ties supported by CPTPP and other agreements.

The European Union recorded exports of about $1.1 billion, growing more than 12% year-on-year, while South Korea reached around $864 million, maintaining steady growth driven by strong demand for squid, octopus, and other marine products.

What the Market Data Reveals

These figures highlight two important structural trends shaping Vietnam’s seafood export strategy.

First, Vietnamese exporters have demonstrated strong market diversification capability, reducing dependence on any single destination. Growth across multiple regions helps mitigate risks from regulatory barriers, trade policy shifts, or demand fluctuations.

Second, free trade agreements are playing a critical role in expanding market access. Agreements such as the CPTPP have significantly improved tariff conditions and created new opportunities for Vietnamese seafood products in high-value markets.

Together, these factors reflect the flexibility of Vietnamese exporters in adjusting product strategies and shipment timing to capture market opportunities. As global seafood trade becomes more competitive and regulated, this ability to adapt quickly will remain a key advantage for Vietnam’s seafood industry.

4. 2026 Outlook: Navigating a Higher-Stakes Environment

Based on forecasts from the Vietnam Association of Seafood Exporters and Producers (VASEP) and early 2026 trade data, Vietnam’s seafood industry is expected to continue growing, although with greater policy and market risks.

Full-Year 2026 Target: Around $11.5 Billion

After reaching a record $11.3 billion in seafood exports in 2025, the industry is aiming for approximately $11.5 billion in 2026. However, exporters will need to navigate a more complex environment shaped by regulatory pressure, shifting demand patterns, and global competition.

Early indicators are mixed. Vietnam’s seafood exports reached about $874 million in January 2026, up 13 percent year-on-year, signaling a relatively strong start to the year.

Key Trends to Watch

1. The Asia–US Divergence Is Becoming Clearer

One of the most noticeable trends in early 2026 is the widening gap between Asian and Western markets.

China has emerged as the largest destination for Vietnamese seafood, with exports reaching nearly $250 million in January 2026, driven by strong demand for premium seafood products ahead of the Lunar New Year.

Japan and South Korea continue to provide stable demand for processed seafood products, particularly shrimp, squid, and pangasius.

By contrast, the United States has become a more challenging market. Seafood shipments to the US fell by nearly 10 percent year-on-year in January, reflecting the impact of tighter regulatory enforcement and trade measures.

Regulations such as the Marine Mammal Protection Act (MMPA), together with anti-dumping duties and certification requirements, are increasing compliance costs and creating uncertainty for exporters.

2. Product-Level Dynamics

Different product categories will face distinct opportunities and challenges in 2026.

Shrimp will likely remain the leading export product. However, shipments to the US may face continued pressure from anti-dumping duties and stricter import regulations. Exporters are increasingly shifting focus toward Asian markets and higher-value shrimp products.

Pangasius remains one of the brightest growth areas. Demand across multiple markets, including ASEAN and CPTPP economies, supports continued expansion. The next major opportunity lies in developing processed pangasius products with higher margins.

Tuna is the most exposed category to regulatory barriers. Compliance with MMPA requirements and certification procedures remains a key challenge for exporters seeking access to the US market.

Cephalopods such as squid and octopus continue to benefit from stable demand in Northeast Asia, particularly Japan and South Korea. Maintaining strict quality standards and traceability will be essential to sustain growth in these markets.

3. February 2026: A Possible Temporary Dip

Despite the strong start in January, exports are expected to slow temporarily in February.

Several factors contribute to this outlook. The Lunar New Year holiday reduces production and shipping activity for many exporters. At the same time, the full impact of US anti-dumping duties on shrimp announced after February 17 could weigh on shipments.

Additional challenges include ongoing difficulties with MMPA compliance and certification requirements for certain seafood products. Meanwhile, Chinese import demand may soften after strong stockpiling in January.

What This Means for Exporters

The overall outlook for Vietnam seafood exports in 2026 remains positive, but the industry is entering a higher-stakes environment.

Growth will depend less on production volume and more on how effectively exporters manage:

- regulatory compliance

- market diversification

- value-added processing

- supply chain transparency

Companies that adapt quickly to these structural shifts will be better positioned to sustain export growth in an increasingly competitive global seafood market.