In 2025, Vietnam attracted a record $38.42 billion in registered foreign direct investment (FDI), with disbursed capital reaching $27.62 billion—the highest level in five years. Early 2026 data already shows strong momentum, with over $6 billion registered in the first two months alone. Yet many foreign investors still lose millions by rushing into the wrong province or misreading local market signals.

Market intelligence and location selection in Vietnam is no longer optional—it is the difference between a thriving operation and a costly relocation within 24 months. This practical guide equips you with a proven, data-driven process to turn raw information into boardroom decisions. Whether you manufacture electronics, assemble automotive parts, or launch a services hub, combining sharp market intelligence and location selection in Vietnam can cut setup risks by 30–40%, reduce operating costs by 20%, and shorten time-to-profit.

Why Market Intelligence and Location Selection in Vietnam Matter More Than Ever

Vietnam’s economy is no longer a simple low-cost story. A young digital-native population, 22 free-trade agreements (including CPTPP and EVFTA), and ongoing supply-chain shifts from China have created a hyper-competitive landscape. Consumer spending is rising 8–10% annually in urban areas, while manufacturing FDI clusters are forming faster than infrastructure can keep up.

Skipping proper market intelligence and location selection in Vietnam leads to predictable failures: factories built in provinces with chronic power shortages, talent pools too thin for scaling, or incentive packages that expire before breakeven. We have seen companies lose 18–24 months and 15–25% of projected ROI simply because they relied on outdated 2023 data or a single government brochure.

Effective market intelligence and location selection in Vietnam delivers three measurable advantages in 2026:

- Risk reduction: Identify regulatory shifts (e.g., new land-use rules in Binh Duong) before signing leases.

- Cost optimisation: Choose locations where land rents range from $80/m² in emerging northern parks to $280/m² near Ho Chi Minh City—matching your exact supply-chain needs.

- Speed to market: Cut licensing timelines from 9 months to under 4 by aligning with provincial priorities.

Ready to enter Vietnam the right way? Contact InCorp Vietnam for a compliance‑first market entry plan.

Step-by-Step Guide to Conducting Market Intelligence in Vietnam

Market intelligence and location selection in Vietnam starts with clear objectives. Begin by answering four questions:

- What is your target customer segment and revenue model?

- Which inputs (components, labour skills, utilities) are most critical?

- What regulatory or incentive thresholds must be met?

- What is your 3-year and 5-year scaling scenario?

Next, collect data across three layers:

Macro intelligence: Track GDP growth (projected 6.5–7% in 2026), inflation (under 4%), and sector forecasts. The General Statistics Office (GSO) and Ministry of Planning and Investment (MPI) publish monthly updates. Focus on your industry: electronics and semiconductors dominate the North, while consumer goods and F&B thrive in the South.

Micro intelligence: Map consumer behaviour by province using Vietnam Household Living Standards Survey data and digital adoption reports from AmCham and EuroCham. Pricing sensitivity in Hanoi differs sharply from Ho Chi Minh City—labour costs in Bac Ninh average 15–20% lower than in Binh Duong, but retention challenges are higher.

Regulatory and incentive intelligence: 2025–2026 incentives remain generous but province-specific. Corporate income tax (CIT) can drop to 10% for 15 years plus 4-year exemptions in high-tech or priority zones. Import-duty exemptions on machinery still apply nationwide for non-locally produced equipment. Always cross-check the latest MPI decrees—policies evolve quarterly.

Practical tools and sources: Use free resources first: MPI’s FDI portal, GSO dashboards, provincial investment promotion centres. Supplement with paid reports from JETRO, World Bank, and local research firms. InCorp Vietnam’s proprietary 5-layer intelligence model (market, competitor, supply-chain, regulatory, risk) compresses 6–8 weeks of desk research into a 10-day actionable report.

Apply a simple PESTLE + SWOT framework tailored to Vietnam. Score each province on a 1–10 scale across your 8 critical factors (detailed below). This turns market intelligence and location selection in Vietnam from guesswork into a repeatable process.

Location Selection Framework: From Strategy to Site in 2026

Market intelligence and location selection in Vietnam succeeds when you evaluate eight non-negotiable factors side-by-side:

1. Proximity to target markets and supply chain: North wins for China-plus-one; South excels for ASEAN and global exports.

2. Labour availability, cost, and skill level: Bac Ninh and Thai Nguyen offer deep electronics talent pools; Central Vietnam provides lower wages but requires more training investment. From January 1, 2026, regional minimum wages increased: Region I (Hanoi, HCMC) now stands at VND5.31 million ($227) per month, Region II (Da Nang, Bac Ninh, Hai Phong, Can Tho) at VND4.73 million ($202), Region III at VND4.14 million ($177), and Region IV at VND3.75 million ($160).

3. Infrastructure and logistics: Hai Phong and Cai Mep ports dominate; new North-South Expressway sections opening in 2026 will reshape Central corridors. Deep-water ports like Lach Huyen and Cai Mep – Thi Vai now apply higher container handling fees: $63–73 per 20-foot and $94–107 per 40-foot container. Container freight rates on key routes have also increased: Hai Phong – HCMC costs 6.5 million VND ($256) per 20-foot, while Hai Phong – Cai Mep costs 7.5 million VND ($295).

4. Investment incentives: Deep C Industrial Park (Hai Phong/Quang Ninh) offers effective CIT around 4.35% for the first 15 years. Many southern parks focus on ready-built factories for speed. The new Law on Digital Technology Industry (effective January 1, 2026) provides full CIT exemption for the first 2 years and a 50% reduction for the following 4 years, along with land rent waivers for 3 years. For semiconductor and high-tech projects, land rent can be waived for up to 22 years with a 57% reduction thereafter.

5. Operating costs: Utilities, land rental ($80–300/m²), and office space vary 30–40% between regions. From January 1, 2026, large customers using 200,000 kWh or more per month will be subject to a new two-component pricing system (capacity and energy prices). The average electricity price per kWh was set at VND 2,204.07 (approx. $0.084), excluding VAT, in May 2025, with an expected 5% increase in 2026.

6. Regulatory and administrative environment: Northern provinces often process licences faster due to experienced FDI teams.

7. Quality of life and talent retention: Da Nang scores highest for expat families; Hanoi and Ho Chi Minh City offer vibrant lifestyles but higher living costs.

8. Risk factors: Flooding in the Mekong Delta, typhoon exposure in Central coast, and occasional power constraints in peak seasons.

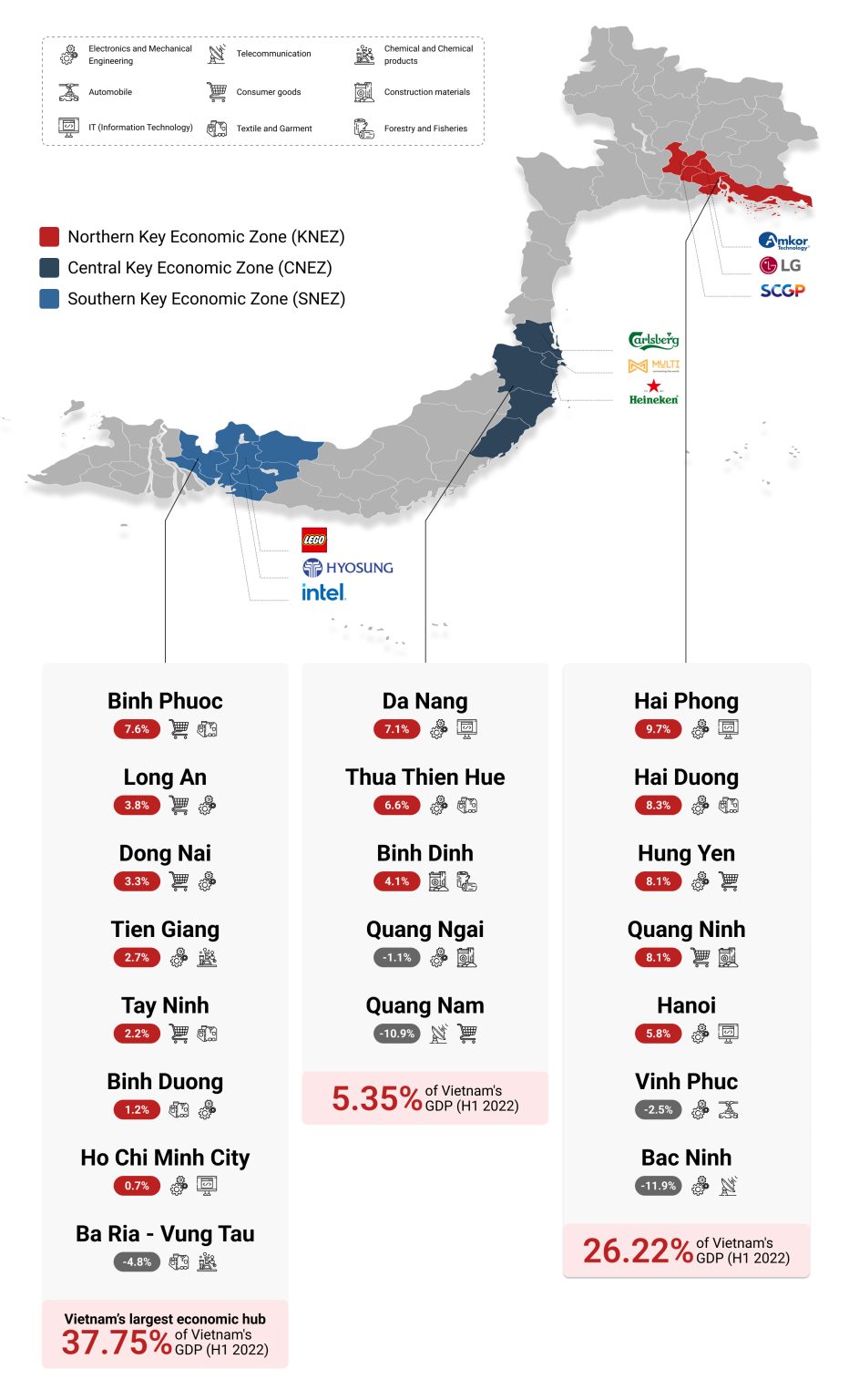

Vietnam’s Major Investment Corridors Compared (2026 Snapshot)

Southern Economic Hub (Ho Chi Minh City, Binh Duong, Dong Nai, Long An)

Mature ecosystem, 90%+ occupancy in top parks (VSIP Binh Duong, Long Hau). Strong port access via Cat Lai and Cai Mep–Thi Vai. Ideal for diversified manufacturing and distribution. Higher costs but fastest scaling. FDI into HCMC industrial parks alone exceeded $5.3 billion in 2025. Dong Nai attracted nearly $550 million in early 2026, with new projects including Cooler Master Vietnam ($100 million) and Sembcorp Integrated Hub Dong Nai ($69.65 million). Average industrial land rent in the South is around $207/sqm/lease term, with HCMC leading at $198/sqm and Binh Duong and Dong Nai accounting for 55% of the region’s supply.

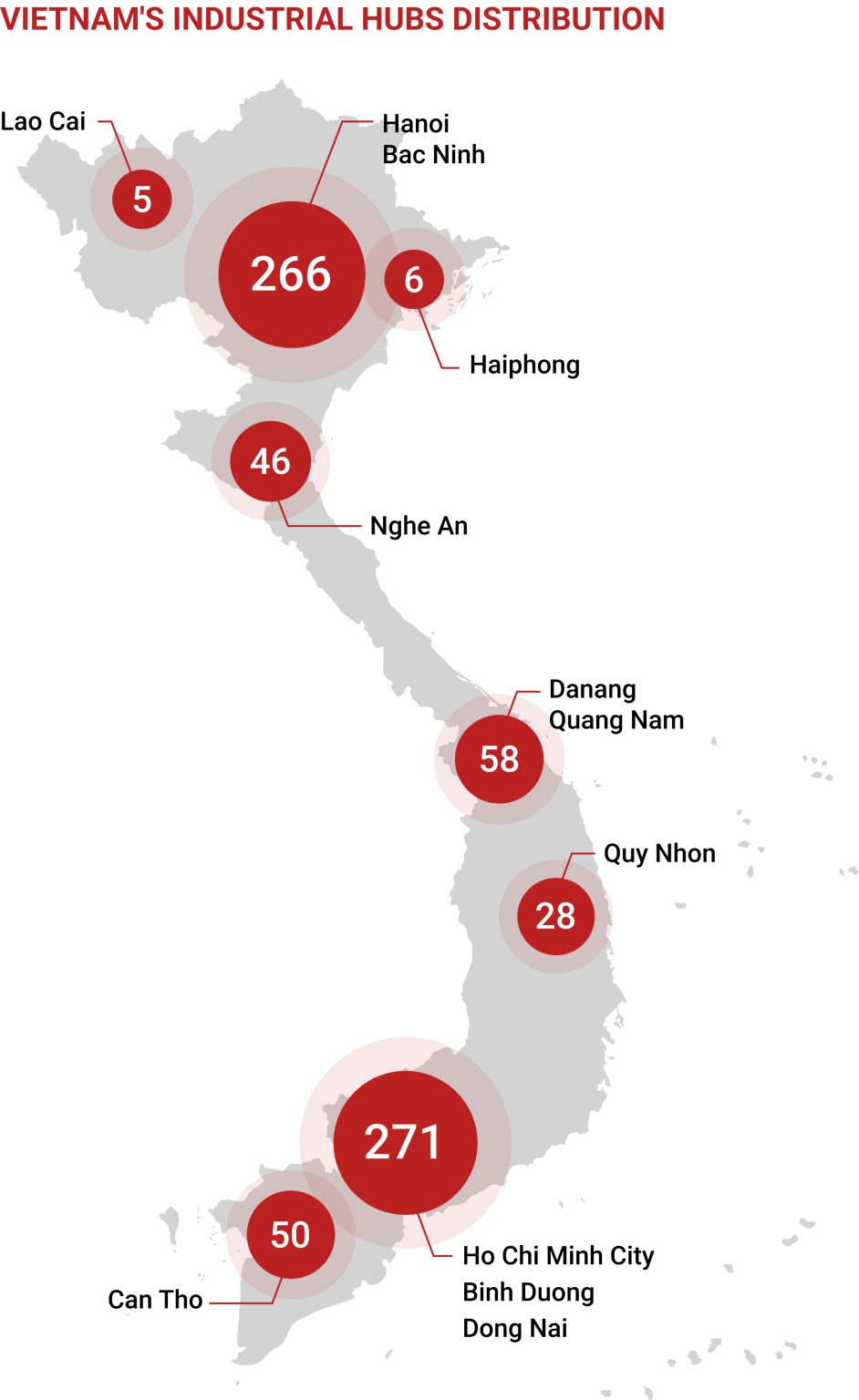

Northern Manufacturing Powerhouse (Hanoi, Bac Ninh, Thai Nguyen, Hai Phong, Quang Ninh)

Electronics and precision manufacturing leader. Proximity to China cuts component logistics by 20–30%. Deep C and VSIP Hai Phong offer massive land banks with aggressive incentives. Labour costs 15–25% lower than South. The North has over 60 active industrial parks, with occupancy rates exceeding 80% in many areas. Bac Ninh Province alone attracted over $18.6 billion in FDI in 2025, ranking among the top two localities in Vietnam. In early 2026, Thai Nguyen greenlit 11 projects worth $1.06 billion, including a major $790 million FDI project. Industrial park land lease prices in the North range from $120–180/m², with clusters at $80–120/m².

Central Growth Corridor (Da Nang, Quang Nam, Quang Ngai)

Emerging sweet spot for 2026. Lower land competition, strong government push for high-tech and renewables. Da Nang Hi-Tech Park and expanded clusters target R&D and green manufacturing. Logistics improving via Lien Chieu port upgrades. Excellent quality-of-life balance. Da Nang attracted $1.33 billion in FDI in early 2026. Quang Ngai currently hosts 62 active FDI projects worth $1.84 billion, with two major industrial parks attracting $18 billion in registered capital. South Korea’s Hyosung has invested over $450 million in the region and is building a new $100 million plant.

Emerging Hotspots

Mekong Delta for agri-processing; Central Highlands for renewables. These suit niche players willing to invest in training and secondary infrastructure. From 2026 onwards, Vietnam is expected to add over 9,000 hectares of new industrial land through more than 30 approved projects. The northern region alone plans to add about 5,050 hectares of industrial land, nearly 1 million square meters of ready-built factories, and over 656,000 square meters of ready-built warehousing between 2026 and 2029.

Top Industrial Parks – Quick 2026 Recommendations:

- Deep C (North): Largest scale, best CIT incentives.

- VSIP network (North & South): Proven management, ready-built options.

- My Phuoc & Bau Bang (Binh Duong): Mature supplier clusters.

- Lien Chieu (Da Nang): Central gateway with hi-tech focus.

Don’t let the legal tsunami catch you off guard. Talk to our team today

Real-World Case Studies: What Actually Works

A European electronics component maker used market intelligence and location selection in Vietnam to choose Bac Ninh over initial interest in Binh Duong. On-ground labour audits revealed 40% higher skilled technician availability in the North. Result: 18-month ramp-up instead of 30, with 22% lower total landed cost thanks to China sourcing.

A Japanese F&B group initially leaned toward HCMC but, after supply-chain mapping, selected Long An. Ready-built factories and Cai Mep port access cut distribution time to key southern markets by 40%. They avoided 6-month delays common in saturated Binh Duong parks.

An Australian renewable-energy firm targeted Central Vietnam after incentive modelling showed 10% CIT + land-tax waivers. Da Nang’s quality-of-life score helped retain expatriate engineers—critical when talent wars intensify in Hanoi and HCMC.

These examples show market intelligence and location selection in Vietnam is not about the “best” province—it is about the best fit.

Common Challenges and How to Overcome Them

Data gaps persist in secondary provinces. Solution: combine GSO numbers with on-site audits (InCorp conducts 2–3 day provincial deep-dives).

Bureaucracy varies—northern provinces are often more FDI-experienced. Mitigate by engaging local investment promotion boards early.

Policy changes happen fast. Build quarterly review triggers into your project timeline.

Land scarcity in prime southern parks reached critical levels in 2025. Secure options 12–18 months ahead or pivot to ready-built solutions.

Power shortages remain a risk. In 2025, Vietnam was affected by extreme weather events, but the government has ensured no electricity shortages for 2025. However, some experts warn of potential power shortages as no major power projects have been implemented in the past decade, and over 170 renewable energy projects remain stalled. Mitigate by evaluating the power supply situation in specific industrial parks and considering backup power solutions.

Compliance with new laws: The Law on Digital Technology Industry (effective January 1, 2026) introduces new incentives but also new requirements for digital technology enterprises. Ensure your investment plans align with this new legal framework.

Conclusion and Actionable Next Steps

Market intelligence and location selection in Vietnam is the foundation of sustainable success in 2026. With FDI momentum continuing and new infrastructure coming online, the window for first-mover advantage remains open—but only for those who combine rigorous data with on-the-ground reality checks.

Vietnam rewards the prepared. Let market intelligence and location selection in Vietnam become your competitive edge.

Learn the Right Setup for Business

Expansion in the Vietnam

Frequently Asked Questions

What is the most common mistake when choosing a province?

- Relying on outdated or brochure-level data. This leads to factories in areas with power shortages or thin talent pools, costing 18–24 months and 15–25% of ROI.

What are the 2026 minimum wages by region?

- From January 2026: Region I (Hanoi/HCMC) $227/month; Region II (Da Nang, Bac Ninh, Hai Phong) $202; Region III $177; Region IV $160. The North averages 15–20% lower labour costs than the South.

What tax incentives are available in 2026?

- High-tech zones offer 10% CIT for 15 years plus 4-year full exemption. The new Digital Technology Law (Jan 2026) adds 2-year full exemption + 4-year 50% reduction. Always verify province-specific rules.

Which industrial parks should I shortlist?

- Deep C (North) for best CIT incentives (~4.35% effective). VSIP for ready-built factories across North & South. Lien Chieu (Da Nang) for hi-tech plus quality of life. Land rents: $80–$280/m².