Service industry in Vietnam has become the country’s main growth engine, both in contribution and economic structure. In 2025, real GDP grew 8.02%, with services expanding by 8.62% and contributing over half of total value-added growth (51.08%), surpassing industry and construction. This signals a clear structural shift toward a service-led economy.

From a business and policy perspective, the sector should be viewed through two lenses. First is the macro shift in structure and labor. Services now account for 42.75% of GDP, while employment has also moved in the same direction, with 40.8% of the workforce in services by Q4 2025. This reflects a gradual transition away from agriculture toward higher-value activities.

Second is the upgrading of market-driven services. Growth is increasingly concentrated in areas where execution and regulatory clarity matter most, including retail, logistics, finance, and hospitality. These segments are expanding rapidly and are closely tied to domestic consumption, tourism recovery, and financial deepening.

For businesses, the service economy in Vietnam is best understood as two interconnected systems. It is a transaction economy driven by payments, logistics, and consumer trust, and a mobility economy shaped by tourism, transport, and urban services. In both, regulation plays a central role. Licensing, tax, data governance, and operational compliance are no longer secondary considerations. They directly affect cost, scalability, and market entry strategy.

Service Industry in Vietnam: The New Engine of GDP Growth

The narrative of Vietnam as solely a “global factory” is evolving. While manufacturing remains a cornerstone, official data signals a structural shift: the service industry in Vietnam has moved from a supporting actor to the economy’s main storyline.

Statistical Snapshot: The “Now” and the Trend

Official releases indicate a powerful upward trajectory for the country. Vietnam’s GDP growth has accelerated from 5.05% (2023) to 7.09% (2024), and is projected to hit 8.02% in 2025.

Within that surge, the value-added growth of the service industry in Vietnam consistently outpaced the general economy, rising from 6.82% in 2023 to 7.38% in 2024 and reaching 8.62% in 2025.

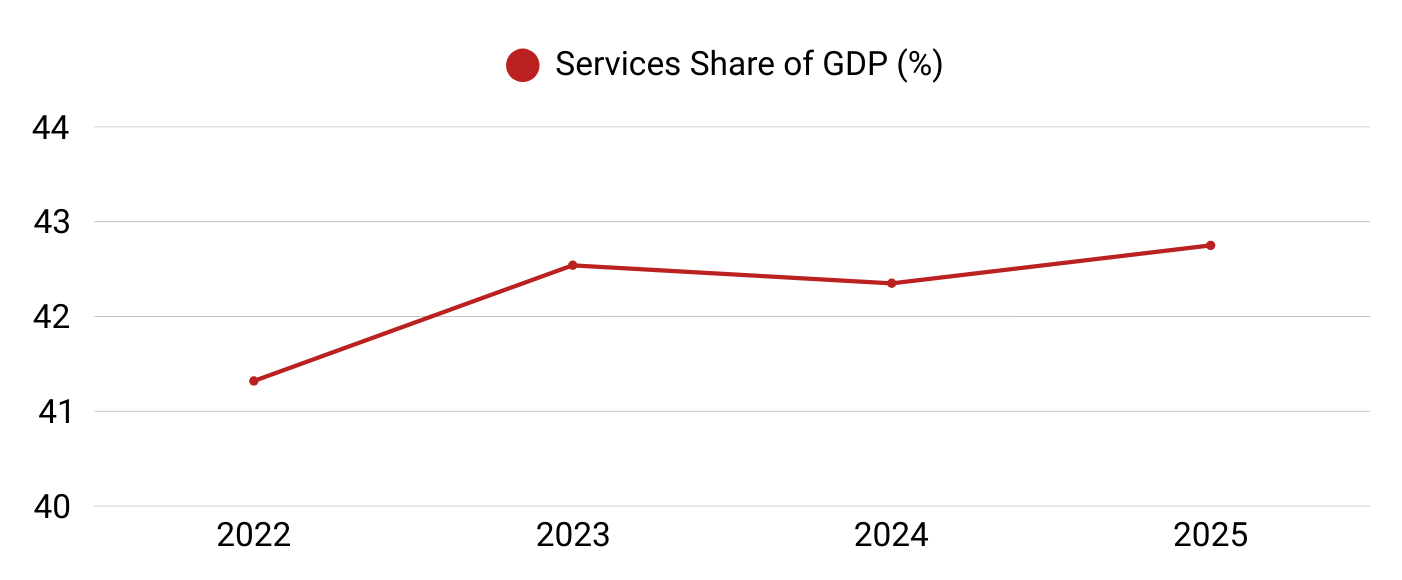

The Structural Shift: Services’ Share of GDP

The share of services in the national GDP has now stabilized above the 42% mark, proving that this sector is a permanent pillar of stability.

Labor Market: Where Quality Meets Growth

By Q4 2025, Vietnam’s employed population reached approximately 52.7 million. The service industry in Vietnam now absorbs 40.8% of that labor force. This concentration makes the sector the primary battleground for debates on job quality, labor absorption, and middle-class expansion.

The Productivity Challenge: Skills vs. Capital

For the business reader, the most critical metric is productivity. In 2025, economy-wide labor productivity was estimated at 245.0 million VND per worker. However, only 29.2% of workers are “trained with degrees/certificates.”

The Insight: Future growth in the service industry in Vietnam is increasingly constrained by skills—specifically in management, digital transformation, and compliance—rather than a lack of capital.

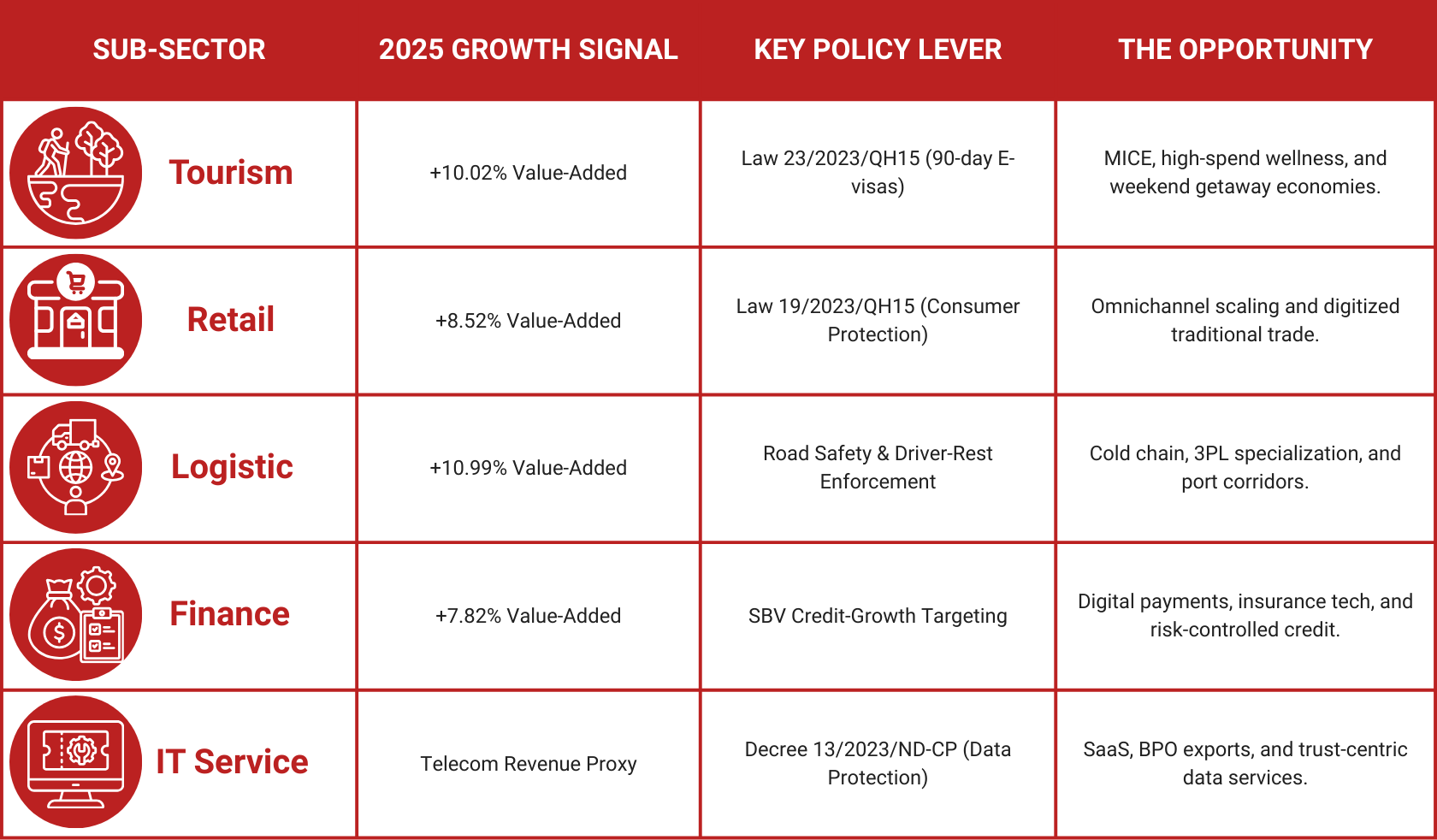

The 2025 Power List: Which Sub-Sectors are Driving the Service Industry in Vietnam?

To provide a truly investable outlook, we must look beneath the “8% GDP” headline. The service industry in Vietnam is not a monolith; it is a collection of high-velocity sub-sectors, each governed by specific new regulations and demand drivers.

In 2025, services accounted for over 51% of Vietnam’s total value-added growth. Here is where that growth is actually happening:

Sub-Sector Deep Dive: Where the Opportunity Lies

The following table breaks down the five pillars of the service industry in Vietnam using the latest official 2025 benchmarks and policy levers.

Visualizing the Drivers: The 2025 Contribution Mix

When we analyze what actually moved the needle for Vietnam’s economy in 2025, the “Market Services” group stands out. While Wholesale & Retail remains the heavyweight, the “Other Services” category—which includes the booming IT and digital backbone—now represents the largest single slice of the service sector’s contribution to growth.

Market Insight: The 8.69% contribution from Transport & Storage (Logistics) is particularly notable. As Vietnam cements its role in global supply chains, logistics has shifted from a cost center to a high-growth value-added engine.

Navigate the service-led shift with ease. From retail to logistics, InCorp Vietnam simplifies your market entry and specialized licensing. Consult our Incorporation Experts to accelerate your 2026 expansion

The Regulatory Roadmap: Navigating Data, Tax, and Trust in the Service Industry in Vietnam

In the service industry in Vietnam, staying ahead isn’t just about market share—it’s about navigating a rapidly evolving legal framework. Over the last 24 months, Vietnam has shifted from general guidelines to specific, board-level compliance requirements that redefine how services are delivered and taxed.

The Regulatory Roadmap (2023–2025)

For any leader in the service industry in Vietnam, these four pillars are now part of the core business model:

- Data as a Liability: Decree 13/2023/NĐ-CP (Effective July 2023) turned personal data protection into a mandatory compliance pillar. Whether you are in Fintech, E-commerce, or Hospitality CRM, mishandling customer data is now a high-stakes legal risk.

- The Consumer Trust Upgrade: Law 19/2023/QH15 (Effective July 2024) drastically strengthens consumer rights. This law puts the burden of responsibility on platforms and marketplaces for dispute resolution and distance selling transparency.

- The Global Tax Shift: Resolution 107/2023/QH15 (Effective January 2024) introduced “top-up” Corporate Income Tax. This aligns Vietnam with global anti-base erosion rules, directly impacting regional HQs and high-value IT/BPO service providers.

- The Mobility Catalyst: Law 23/2023/QH15 (Effective August 2023) extended e-visas to 90 days (multiple entry). This is a massive structural tailwind for MICE tourism and the broader visitor economy.

The “Urban Services” Pulse

For those in property-adjacent services (real estate tech, facility management), the Ministry of Construction has begun providing more frequent, data-driven signals. In 2025, official housing indices have replaced anecdotes, allowing for more grounded “urban service” narratives in your business planning.

Key Takeaway: In the service industry in Vietnam, the “Regulatory Milestone” is your best predictor of where the next market opportunity—and the next audit risk—will appear.

From Growth to Governance: Navigating the 3 Main Friction Points in the Service Industry in Vietnam

Despite global policy shifts, the service industry in Vietnam remains the economy’s most resilient feature. While the World Bank’s Taking Stock report (March 2025) cautiously forecasted real GDP growth at 6.8% for 2025 and 6.5% for 2026, the sector continues to outperform these baselines due to a massive “mix-shift” in domestic consumption.

Key Trends: The Leapfrog Effect

According to analysis by McKinsey & Company, Vietnam is experiencing a “leapfrog” moment. We aren’t just seeing more shops; we are seeing the digitization of traditional trade. E-commerce and modern retail formats are merging, creating a “sticky” post-pandemic behavior where digital-first services are no longer optional—they are the standard.

Navigating the Friction: 3 Critical Challenges

Growth in the service industry in Vietnam comes with new operational hurdles that firms must clear to remain profitable:

- Compliance Intensity: Rising standards in data and consumer protection (Decree 13 and Law 19) have increased fixed costs. However, early adopters of strong governance are gaining a significant “trust premium” in the market.

- Logistics Execution: It’s no longer just about building roads. Stricter enforcement of transport rules and driver-rest regulations is shifting cost structures, making regulatory execution a core part of logistics competitiveness.

- Credit Sensitivity: The State Bank of Vietnam’s (SBV) cautious stance on real estate exposure directly impacts service expansion. Whether you are rolling out a retail chain or a hotel group, financing cycles are now more tightly linked to macro-risk controls.

The Opportunity: A Record-Breaking Recovery

The most visible win for the service industry in Vietnam is the tourism rebound. From 12.6 million international arrivals in 2023, government reporting for 2025 suggests a surge to 22–23 million visitors. This isn’t just a recovery; it’s a total expansion of the “visitor economy,” fueled by the 90-day e-visa reforms.

Don’t let new regulations stall your growth. Our specialists ensure your data, tax, and operational models are fully compliant and audit-ready. Book a Compliance Health Check with InCorp Vietnam today.

From Policy to P&L: Actionable Strategies for 2026

1. Capture the “Channel + Fulfillment” Loop

In 2025, the service industry in Vietnam contributed 51.08% to total value-added growth, driven largely by Wholesale/Retail and Transport/Storage.

- Business Action: Stop treating logistics as a back-office cost. If you are expanding retail or e-commerce, treat 3PL contracting, routing efficiency, and inventory discipline as core components of your store economics.

- Policy Signal: Competitive advantage now belongs to those who master the physical delivery of the digital promise.

2. Pivot to the “High-Spend” Visitor Economy

With international arrivals jumping from 12.6M (2023) to an estimated 22–23M (2025), the 90-day e-visa (Law 23/2023/QH15) has fundamentally changed the traveler profile.

- Business Action: Repackage offerings for “Long-Stay” segments and MICE (Meetings, Incentives, Conferences, and Exhibitions). Invest in multilingual customer operations and robust fraud controls for international payments.

- Policy Action: Treat visa policy as a “services export strategy” by publishing corridor-level performance dashboards (spend, seasonality, and flight data).

3. Turn Data Governance into a Sales Tool

Decree 13/2023 (Data Protection) is often seen as a hurdle, but in the service industry in Vietnam, it is a trust differentiator.

- Business Action: Implement a “Minimum Viable Privacy Program” (data inventory and breach playbooks) before scaling personalized marketing. Use superior data ethics to reduce churn and lower reputational risk in Fintech and E-Commerce.

- Policy Action: Seek clearer sector-specific playbooks from authorities to reduce uncertainty-driven underinvestment.

4. Professionalize Operations via Consumer Protection

Law 19/2023/QH15 (Effective July 2024) significantly raises the bar for platform responsibility and dispute resolution.

- Business Action: Create measurable SLAs for refunds and transparency. In the service industry in Vietnam, “Trust” is now a regulated metric. Ensure fee structures and delivery windows are communicated with $100\%$ transparency to avoid MOIT (Ministry of Industry and Trade) penalties.

5. Stress-Test Growth Against the “Hidden Governor” (Credit)

As of early 2026, the State Bank of Vietnam maintains a cautious stance on credit growth, particularly regarding real estate exposure.

- Business Action: Stress-test your expansion plans (new warehouses, hotel capex, or retail rollouts) against credit-tightening scenarios. Diversify your funding through supplier finance or strategic equity rather than relying solely on bank debt.

6. Optimize for the FDI Accelerator

With 2025 seeing the highest disbursed FDI in five years ($27.6B), the demand for “FDI-ready” local services is peaking.

- Business Action: If you provide IT, HR, or Facility Management, productize your offerings with bilingual contracting, KPI dashboards, and international compliance packages.

- Policy Action: Track and publish “Service-Supplier Readiness” metrics in industrial corridors to help local firms capture more value from FDI clusters.

Learn the Right Setup for Business

Expansion in the Vietnam

Frequently Asked Questions

How big is the service sector today?

- It is now Vietnam's primary growth engine, accounting for 42.75% of GDP and contributing over 51% of total value-added growth in 2025. It has officially surpassed industry and construction in economic contribution.

Which sub-sectors offer the most opportunity?

- High-growth winners include Logistics (+10.99%), Tourism (+10.02%), and Retail (+8.52%). These are driven by 90-day e-visas, digitized supply chains, and a booming middle class.

What are the "must-know" regulations for 2026?

- Two laws are critical: Decree 13 (Data Protection), which requires mandatory audits for customer data, and Law 19 (Consumer Protection), which holds platforms liable for disputes and transparent pricing.

What is the biggest operational hurdle?

- The skills gap. While the sector absorbs 40.8% of the workforce, only 29.2% are formally trained. Success depends on investing in management and digital systems rather than just adding headcount.