If you are a foreign investor planning to launch a new business venture in Vietnam, navigating the local corporate tax landscape is likely at the very top of your priority list. Recently, the Vietnamese business community has been abuzz regarding a highly attractive financial incentive: a 3-year corporate income tax (CIT) break for newly established small and medium-sized enterprises (SMEs).

For any new venture, legally bypassing Vietnam’s standard 20% corporate tax rate during the critical first 36 months of operation is a massive competitive advantage. Securing a multi-year tax exemption can make the difference between a startup that struggles to survive its initial cash-burn phase and one that successfully reinvests its pre-tax profits into hiring top talent, aggressive marketing, and rapid scaling.

But for a brief, tense period in early 2026, foreign investors were left in a state of regulatory limbo. The question echoing through boardrooms from Ho Chi Minh City to Hanoi was simple: Does your new Foreign Direct Investment (FDI) startup actually qualify for this tax exemption?

Conflicting rulings from provincial authorities temporarily suggested that FDI startups might be entirely excluded from this benefit. Fortunately, the General Department of Taxation has definitively stepped in. With the rapid issuance of Official Letter 3897/CT-CS (and its companion, 3896/CT-CS) in June 2026, the debate is officially over, and the outcome is highly favorable for international business owners.

The Origin of the Incentive: The Foundational Laws

To fully appreciate the power and relief brought by Official Letter 3897, we must first look at the foundational laws that created this tax exemption. The Vietnamese government has consistently shown a commitment to modernizing its economy, and recent legislation reflects a strong drive to stimulate early-stage entrepreneurship.

Resolution 198/2025/QH15

Adopted by the National Assembly on May 17, 2025, this resolution established special mechanisms to support private economic development. Crucially, under Article 10, Clause 4, the resolution explicitly states:

“Small and medium-sized enterprises shall be exempt from corporate income tax for 03 years from the date of first issuance of the Enterprise Registration Certificate.”

Decree 20/2026/ND-CP

To provide actionable, real-world guidelines for the resolution, the Government issued Decree 20/2026/ND-CP in January 2026. Under Article 7, Clause 3, the decree further clarified the mechanics of the incentive, stating that the exemption period is calculated continuously from the first year the Enterprise Registration Certificate (ERC) is issued.

The Practical Takeaway: The clock on your tax exemption starts ticking the moment your company is officially registered and incorporated. It does not wait for your startup to generate its first dollar of revenue or become profitable. Incorporating this timeline into your initial financial forecasting is an absolute necessity.

Read More: Register Company in Vietnam: Step-by-Step Guide

The Short-Lived Crisis: Why Were FDIs Being Excluded?

Despite the clear, supportive language in the foundational decree, a major regulatory roadblock appeared for foreign investors in the first half of 2026.

Because Resolution 198 specifically referenced “private economic development,” several provincial tax departments interpreted the law in a highly restrictive manner. Officials—most notably through initial rulings in Ho Chi Minh City and later formalized in Tay Ninh via Official Letter 5620/TNI-QLDN1—argued that the tax exemption was intended solely for domestic private companies, legally isolating the foreign-invested sector.

Virtually overnight, legitimate FDI startups were being told they did not qualify for the 3-year tax exemption. This caused widespread concern, paused capital injections, and forced strategic pivots among the international business community, as a 20% hit to early-stage corporate income radically alters a startup’s financial modeling.

The Game-Changer: Enter Official Letter 3897/CT-CS

Recognizing the severe chilling effect this local misinterpretation could have on foreign direct investment, the General Department of Taxation in Hanoi took decisive action.

On June 11, 2026, they issued unified, national-level guidance through Official Letter 3897/CT-CS and Official Letter 3896/CT-CS. These documents effectively revolutionized the conversation, overruled the restrictive provincial interpretations, and firmly secured the tax exemption for foreign investors.

The national ruling was crystal clear and unambiguous:

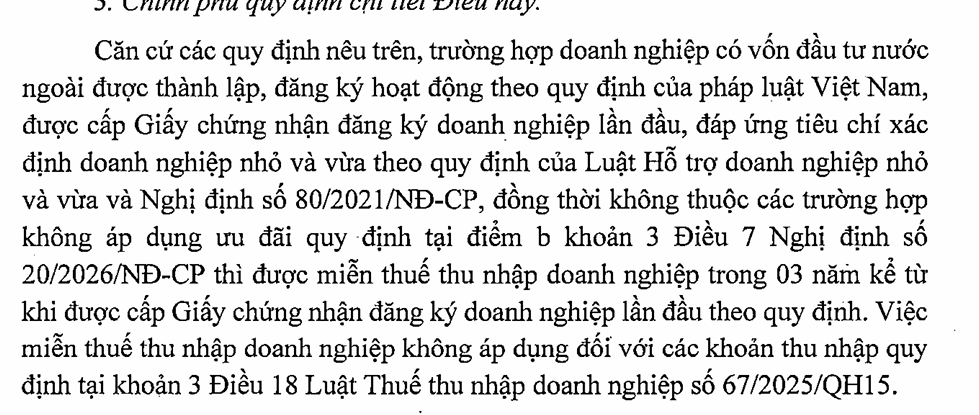

“Foreign-invested enterprises (FDI) are not excluded from the scope of application for CIT exemption incentives, provided that they fully meet the conditions for newly established small and medium-sized enterprises as prescribed.”

Furthermore, Official Letter 3897 explicitly suspended the previous restrictive guidance from local departments that had attempted to block FDI eligibility.

The Final Verdict: Thanks to this definitive ruling, your FDI enterprise absolutely CAN qualify. Your status as a foreign-owned entity does not disqualify you from this tax exemption. However, the government’s generosity comes with strict compliance strings attached. You must meticulously meet the legally prescribed conditions.

The Eligibility Checklist: How to Secure Your Incentive

While Official Letter 3897 opened the door, walking through it requires precise corporate structuring and foresight. To successfully claim the 3-year tax exemption, your new FDI enterprise must satisfy all three of the following critical conditions. Do not assume your startup automatically qualifies just because it is new.

Condition 1: You Must Genuinely Qualify as an SME

The Vietnamese government relies on strict numerical thresholds to define what constitutes a Small and Medium-Sized Enterprise. To qualify, your startup must meet the following metrics:

- The Employee Threshold: The average annual number of employees participating in Vietnam’s mandatory state social insurance system must not exceed 200 people.

- The Financial Thresholds (You must meet at least ONE of these):

- Your Total Capital Fund does not exceed 100 billion VND (approximately USD 4 million).

- Your Total Revenue of the preceding year does not exceed 300 billion VND (approximately USD 12 million).

Incorp Vietnam Insight: Capital structure is everything during incorporation. If you are launching an FDI with a massive initial charter capital injection of USD 5 million, you will immediately break the capital threshold and disqualify yourself from this specific tax exemption. We highly recommend structuring your initial capital strategically to stay within the SME parameters if this tax break is a priority for your financial roadmap.

Condition 2: First-Time Business Registration

This incentive is strictly designed to spur new business creation and broaden the tax base over the long term. Therefore:

- Your enterprise must be registering for business for the very first time.

- You must be a newly established, formal legal entity.

Condition 3: Avoiding the “Excluded Categories”

This is the most dangerous pitfall for foreign investors. Even if your FDI is a newly registered SME that perfectly meets the size thresholds, you will completely lose the tax exemption if your business structure triggers either of the government’s strict anti-abuse clauses:

1. The Restructuring Trap (Category A)

Tax authorities will not grant a tax break to an “old” business wearing a “new” mask. If your company is formed through a merger, consolidation, division, separation, ownership transfer, or a conversion of enterprise type, you are categorically excluded.

2. The “Recycled Management” Rule (Category B)

This clause is vital for serial entrepreneurs to understand and navigate carefully. You are excluded if your newly established enterprise has a Legal Representative (unless they are merely a hired manager with zero capital contribution), a partner, or a highest capital-contributing member who has previously held those same leadership or ownership roles in:

- A currently operating enterprise in Vietnam, OR

- An enterprise in Vietnam that was dissolved less than 12 months ago.

Case Study Example: Imagine you are a foreign investor who was the highest capital contributor of an underperforming logistics company in Hanoi, which you officially dissolved in January 2026. If you set up a brand new, unrelated tech FDI in Ho Chi Minh City in July 2026, your new company is completely disqualified from the tax exemption because your previous company was dissolved less than 12 months prior. The government views this as “recycled management.”

Not sure if your planned capital structure or founding team meets the strict conditions for the 3-year tax exemption? 👉 Book a Free Tax Structuring Consultation with Incorp Vietnam Today

Practical Scenarios: Maximizing Your FDI Tax Strategy

How do these national regulations translate to your real-world market entry? Let us look at three common scenarios our advisory team handles at Incorp Vietnam.

Scenario 1: You Meet All Conditions – Congratulations!

If your startup meets the SME criteria, is a genuine first-time registration, and carefully avoids the excluded categories, you have unlocked one of Vietnam’s most powerful financial incentives.

Your Action Plan:

- Proactive Filing is Mandatory: Tax breaks in Vietnam are not applied automatically by the authorities. You must work with your corporate service provider to ensure your chief accountant formally applies for and documents your eligibility for the tax exemption in your annual tax finalization reports.

- Vetting Representatives: Before legally appointing a General Director or Legal Representative, conduct a thorough background check on their Vietnamese corporate history. Ensure they do not trigger the “Recycled Management” exclusion, which would penalize your entire organization.

- Document Everything: Maintain pristine records proving your SME status, specifically tracking registered capital contributions and the exact number of employees registered on the state social insurance platform.

Scenario 2: You Do Not Qualify for the SME Incentive

If your FDI project simply must exceed the 100 billion VND capital limit, or if you run foul of the “Recycled Management” rule due to past ventures, do not panic. Vietnam’s foreign investment landscape offers a variety of alternative tax exemption avenues:

- Project-Based Incentives (Decree 218/2013/ND-CP): Depending on your specific business sector and geographic location, you might qualify for equally impressive incentives. New investment projects located in high-tech parks, economic zones, or socio-economically disadvantaged areas can receive up to 4 years of total CIT exemption, followed by a 50% tax reduction for the next 9 years, alongside preferential long-term rates of 10%.

- Priority Sectors: Projects engaged in software production, renewable energy, advanced manufacturing, healthcare, and education have their own highly lucrative tax exemption frameworks designed to attract foreign capital.

- Double Taxation Avoidance Agreements (DTAAs): If your corporate structure involves heavy cross-border transactions, leveraging Vietnam’s extensive network of DTAAs can result in specific tax relief, reductions, or refunds on withholding taxes.

Scenario 3: Navigating Transitional Timelines

Because Official Letter 3897 was only recently issued in June 2026, some businesses currently find themselves caught in a transitional grey area:

- What if you established your FDI company in March 2026, during the brief window when local authorities were denying the exemption? The great news is that under the new national guidance, as long as you legally meet the SME criteria, you can still claim the tax exemption for the remainder of your 3-year period. The General Department of Taxation’s ruling decisively overrides any previous local rejections. You have not lost your window of opportunity.

Let our local experts handle the bureaucracy. From initial business registration to securing your tax incentives and managing your monthly accounting, Incorp Vietnam provides end-to-end corporate solutions.

Key Takeaways for Foreign Investors

As you prepare to launch, structure, or scale your business operations in Vietnam, keep these core principles regarding Official Letter 3897 firmly in mind:

- FDIs are Officially Eligible: Official Letter 3897/CT-CS is your ultimate legal shield. It confirms definitively that the 3-year CIT incentive is available to foreign-invested enterprises.

- Size is Everything: Your FDI status alone does not guarantee the benefit; your corporate size does. Keep your initial registered charter capital under 100 billion VND and your formal headcount under 200 to maintain your SME status.

- Audit Your Founders: Treat the corporate history of your founding team, major shareholders, and legal representatives with the utmost seriousness to avoid the disastrous “recycled management” disqualification.

- The Clock Does Not Wait: Your 3-year incentive period begins the exact moment you receive your Enterprise Registration Certificate. Incorporate this strict timeline into your operational and financial forecasting immediately so you do not waste months of your exemption period on administrative setup.

How Incorp Vietnam (An Ascentium Company) Can Secure Your Tax Advantage

Navigating Vietnam’s dynamic corporate tax environment requires far more than simply reading the law—it requires strategic foresight, flawless execution, and a deep, practical understanding of how local tax authorities interpret new national guidelines like Official Letter 3897.

The Vietnamese government’s intent with this policy is clear: they want to actively support genuine, newly established businesses—whether domestic or foreign-invested—while simultaneously preventing tax avoidance through “phoenix” companies or constant corporate restructuring.

Do not leave your startup’s financial future to chance or misinterpretation.

At Incorp Vietnam (an Ascentium company), our dedicated team of seasoned tax advisors, legal experts, and corporate secretaries specialize in guiding foreign investors safely through every single step of the market entry process. From structuring your initial charter capital to ensure maximum eligibility for a tax exemption, to vetting your executive team, handling your ongoing compliance, and executing flawless tax finalization, we are your trusted, on-the-ground partners in Vietnam.

Are you ready to set up your FDI entity in Vietnam with absolute confidence? Contact the experts at Incorp Vietnam today for a comprehensive, personalized business consultation. Let us handle the complex regulatory landscape so you can focus entirely on what matters most: building a highly successful, scalable business in Southeast Asia’s most dynamic and exciting economy.

Learn the Right Setup for Business

Expansion in the Vietnam

Frequently Asked Questions

Can a Foreign Direct Investment (FDI) startup legally claim the 3-year tax exemption?

- Yes. Official Letter 3897 definitively confirms that foreign-invested enterprises are fully eligible for the 3-year tax exemption, provided they meet the legal criteria for a newly established Small and Medium-Sized Enterprise (SME).

What exact size limits must my startup stay under to qualify?

- To secure the tax exemption, your startup must have under 200 employees (on state social insurance) AND meet at least one of these financial limits: registered capital under 100 billion VND (approx. USD 4 million) OR prior year's revenue under 300 billion VND (approx. USD 12 million).

I closed down a company in Vietnam recently. Will this disqualify my new startup?

- Yes. Under the "recycled management" rule, if your new company's Legal Representative or highest capital-contributing partner dissolved a Vietnamese business within the last 12 months, your new startup is instantly disqualified from the tax exemption.

Does the 3-year exemption clock start only after my business becomes profitable?

- No. The 3-year clock starts continuously on the exact date your Enterprise Registration Certificate (ERC) is issued—not when you generate revenue. Additionally, the tax exemption is not automatic; your accounting team must proactively claim it during your annual tax finalization.