Vietnam is transitioning from Vietnamese Accounting Standards (VAS) to International Financial Reporting Standards (IFRS), a major shift affecting how businesses report financial information, particularly in the context of IFRS and VAS in Vietnam. This article will help you understand the key differences between VAS and IFRS and prepare for the upcoming changes. Many companies are also consulting accounting and taxation services experts to smoothly adapt to IFRS compliance and ensure accurate financial reporting during this transition.

Understanding IFRS and VAS in Vietnam

The International Financial Reporting Standards (IFRS), developed by the International Accounting Standards Board (IASB), serve as a global accounting language adopted by companies in over 140 jurisdictions worldwide. With more than 160 countries and territories incorporating IFRS into their financial reporting frameworks, these standards have become instrumental in enhancing the credibility and comparability of financial information globally.

On the other hand, Vietnamese Accounting Standards (VAS) were specifically designed to address the local economic and regulatory landscape. Issued by the Ministry of Finance, these standards have been continuously revised to incorporate emerging best practices and align with international accounting standards. VAS originated from older versions of the International Accounting Standards (IAS) and aims to meet the unique requirements of businesses operating in Vietnam, adhering to the accounting standard.

Vietnam’s accounting landscape is undergoing significant transformation with the adoption of IFRS. The Vietnamese government’s strategic plan to adopt IFRS by 2025 aims to integrate these practices into financial markets, enhancing transparency and comparability in corporate financial statements. This shift aligns Vietnamese financial reporting standards (VFRS) with global practices, fostering greater investor confidence and attracting foreign investments.

Read Related: Vietnam Business Accounting & Taxation: Principles of Taxation, Problems & Solutions, and Accounting Department Setup

Key Differences Between IFRS and VAS

When comparing IFRS and VAS, several key differences emerge, fundamentally affecting how financial information is reported and interpreted. With its broader coverage and specific guidelines, IFRS emphasizes flexibility and transparency, contrasting sharply with the more rigid, rules-based approach of VAS.

The following subsections will explore these differences, exploring the principles-based versus rules-based approach, historical cost versus fair value measurement, and revenue recognition.

Principles-Based vs. Rules-Based Approach

One of the fundamental differences between IFRS and VAS lies in their respective approaches to financial reporting. IFRS uses a principles-based approach. This method provides greater flexibility while striving for high transparency and comparability. This approach allows businesses to adapt their financial reporting based on underlying principles, particularly useful in complex and evolving financial transactions.

In contrast, VAS adopts a rules-based approach, mandating strict adherence to standardized formats and specific rules. This rigidity leaves little room for interpretation, often resulting in a more straightforward but less adaptable financial reporting process.

IFRS’s principles-based approach aligns better with modern financial complexities, whereas VAS’s rules-based framework may limit its applicability in dynamic financial environments.

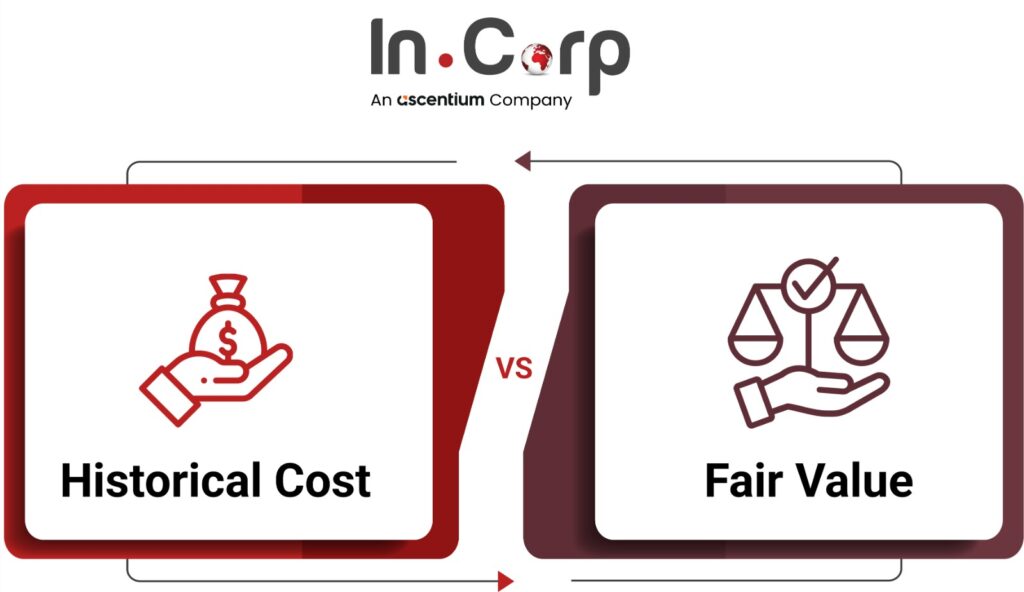

Historical Cost vs. Fair Value Measurement

Under IFRS and VAS in Vietnam, a key distinction lies in how assets and liabilities are measured. Under VAS, the historical cost principle is predominantly applied, meaning assets and liabilities are recorded at their original acquisition cost. While this method offers consistency, it may not accurately reflect current market conditions—potentially limiting the real-time relevance of financial statements.

In contrast, IFRS, as part of the evolving framework of IFRS and VAS in Vietnam, emphasizes fair value measurement. This approach ensures that financial reports present a more accurate and timely picture of an entity’s financial position, especially in dynamic or volatile markets. The focus on fair value enhances transparency and decision-making for stakeholders, making IFRS more responsive to today’s global business environment.

Revenue Recognition

Revenue recognition under IFRS is governed by IFRS 15, which requires revenue to be recognized when control of a good or service transfers to a customer. This standard introduces a five-step process for revenue recognition, promoting consistency and clarity in financial reporting. The principles-based framework of IFRS ensures that revenue is recognized in a manner that reflects the economic substance of transactions.

On the other hand, VAS 14 and VAS 15 are based on older versions of IAS and provide conditions for recognizing revenue without a comprehensive model. These standards include specific guidelines on revenue allocation and matching, which can result in variations in practice and potentially less consistency in financial reporting.

The shift to IFRS 15 offers a more robust and transparent framework for revenue recognition.

Discover more Accounting Services & Tax Reporting Outsourcing in Vietnam

Transitioning from VAS to IFRS

The transition from VAS to IFRS is a strategic move by the Vietnamese government to align corporate financial reporting with international best practices. This transition is structured into two main phases: the Voluntary Application phase (2022-2025) and the Compulsory Application phase (post-2025).

The subsequent phases will outline the steps businesses need to take for a smooth transition.

Phase I: Voluntary Application (2022-2025)

The voluntary application phase serves as a critical preparatory stage in the broader transition toward IFRS and VAS in Vietnam alignment. During this period, state-owned enterprises, listed companies, and large public firms are encouraged to voluntarily adopt IFRS. This allows organizations to gradually adjust their accounting practices and systems, and begin aligning financial reporting with international standards under the evolving IFRS and VAS in Vietnam framework.

Businesses that embrace this phase can proactively address technical and resource-related challenges, ensuring a smoother transition when IFRS becomes mandatory. Early adoption not only demonstrates leadership but also contributes to raising overall market readiness for IFRS and VAS in Vietnam compliance.

Phase II: Compulsory Application (Post-2025)

From 2025 onward, the adoption of IFRS will become mandatory for specified enterprises, requiring them to prepare consolidated financial statements in accordance with IFRS standards. This marks a significant milestone in the reform of IFRS and VAS in Vietnam, signaling a national commitment to aligning with global accounting practices and enhancing financial transparency.

Successful compliance will demand comprehensive planning, upgrades to accounting systems, and extensive training for finance teams. As Vietnam moves toward full implementation, a deep understanding of IFRS and VAS in Vietnam will be essential for navigating the changes and ensuring regulatory alignment.

Challenges and Solutions in Adopting IFRS

Transitioning from VAS to IFRS presents a number of challenges for businesses operating within the evolving landscape of IFRS and VAS in Vietnam. Key obstacles include organizational readiness, limited resources, and access to accurate and timely information. Companies must adapt existing accounting practices, ensure compliance with new standards, and provide extensive training for their finance teams to align with the dual reporting expectations under IFRS and VAS in Vietnam.

Training and Capacity Building

One of the most pressing issues in the transition to IFRS and VAS in Vietnam is the complexity of IFRS standards and their significant departure from VAS. Many organizations struggle with limited financial and human resources, which can hinder effective implementation. Specialized training programs are essential—not only to build technical knowledge but also to develop the practical skills needed for preparing IFRS-compliant financial statements. Hands-on case studies and real-world applications play a vital role in helping professionals understand and apply IFRS in the context of IFRS and VAS in Vietnam.

System and Process Upgrades

A smooth transition also requires significant upgrades to internal systems and accounting software. To comply with IFRS and VAS in Vietnam, businesses often implement dual ledger systems and adjust their Chart of Accounts to accommodate the differing requirements of each standard. These upgrades demand time, investment, and strategic execution to avoid disruption to financial reporting.

By proactively addressing these challenges—with training, system readiness, and compliance planning—businesses will be better positioned for a successful transformation under the IFRS and VAS in Vietnam framework.

Benefits of Adopting IFRS in Vietnam

Adopting IFRS enhances the transparency and comparability of financial statements, offering stakeholders more reliable and relevant financial information. Within the framework of IFRS and VAS in Vietnam, this increased transparency fosters stronger investor confidence, attracting more foreign investments and promoting improved corporate governance and accountability.

Aligning Vietnam’s financial reporting system with international standards through IFRS and VAS in Vietnam reforms also simplifies the reporting process for multinational corporations operating locally. Transitioning to IFRS contributes to broader economic efficiency by improving capital allocation, reducing reporting costs, and aligning Vietnam more closely with global financial markets. For both Vietnamese businesses and the overall economy, adopting IFRS under the evolving IFRS and VAS in Vietnam agenda presents substantial strategic and operational benefits.

Specific Areas of Difference in Financial Reporting

Several specific areas of financial reporting differ significantly between IFRS and VAS, directly impacting how financial statements are structured and interpreted. These distinctions are critical in the context of IFRS and VAS in Vietnam, especially for organizations preparing to adopt IFRS.

Presentation of Financial Statements

Under IFRS, companies enjoy flexibility in designing their financial statements, allowing for a format that better reflects the nature of their business. The statement of changes in equity is presented separately, and expenses may be shown by either nature or function—enhancing the clarity and relevance of reporting. In contrast, VAS prescribes rigid standardized formats. For example, under VAS 21, expenses must be presented strictly by function, limiting the scope for meaningful presentation adjustments.

Asset Impairment

One of the most notable differences between IFRS and VAS in Vietnam is the approach to asset impairment. IFRS requires immediate recognition when an asset’s fair value falls below its carrying amount, ensuring that financial reports reflect current economic realities. VAS, however, lacks detailed guidance on asset impairment, leading to inconsistencies and potential inaccuracies in reporting. The IFRS model, with its fair value-based approach, provides a more accurate picture of an entity’s financial health—further underscoring the importance of transitioning under IFRS and VAS in Vietnam reforms.

Deferred Tax Liabilities

IAS 12 under IFRS requires entities to recognize a deferred tax liability for all temporary differences, with specified exceptions. This comprehensive approach ensures deferred tax liabilities are accurately reflected in financial statements, providing a clearer picture of the entity’s financial position.

VAS 17 has limitations regarding the recognition of deferred tax liabilities, particularly concerning temporary differences. This can result in inconsistencies and less comprehensive financial reporting. IFRS adoption addresses these gaps, offering a more robust framework for recognizing deferred tax liabilities.

The Future of Financial Reporting in Vietnam

The future of financial reporting in Vietnam is set to be significantly shaped by the adoption of International Financial Reporting Standards (IFRS). As Vietnam transitions to IFRS, the country is poised to enhance its integration into the global economy, aligning its financial reporting standards with international best practices. This alignment will not only improve the transparency and comparability of financial information but also attract foreign investments and foster greater investor confidence.

The implementation of IFRS will also promote better corporate governance and accountability, as businesses will be required to adhere to more stringent and transparent financial reporting standards. This shift will necessitate a comprehensive overhaul of internal processes and systems, ensuring that companies are well-prepared to meet the new requirements. The journey towards full IFRS adoption will undoubtedly present challenges, but the long-term benefits for the Vietnamese economy and its businesses are substantial.

Looking ahead, Vietnam’s financial reporting landscape will continue to evolve as the country embraces IFRS. The successful adoption of these standards will position Vietnam as a competitive and attractive destination for international investors, ultimately contributing to the country’s economic growth and development.

Businesses and financial professionals must stay informed and proactive to navigate this transition effectively and capitalize on the opportunities it presents.

How InCorp Can Help?

Vietnam’s move to international financial reporting standards (IFRS) changes how businesses handle their finances. Knowing the differences between current local rules (VAS) and IFRS is key for any company operating here. IFRS focuses on general principles, while VAS uses specific rules, which means businesses need to adapt their thinking.

Incorp Vietnam assists businesses throughout this transition. We provide guidance on understanding IFRS, developing transition plans, and ensuring compliance. We help businesses adapt their systems and train their staff, making the switch smoother and more efficient. By partnering with Incorp Vietnam, businesses can confidently navigate the shift to IFRS and take advantage of the opportunities it creates. Connect with Incorp Vietnam to learn how we can support your IFRS transition.

clients worldwide

professional staff

incorporated entities in 10 years

compliance transactions yearly

Learn the Right Setup for Business

Expansion in the Vietnam

Frequently Asked Questions

Does Vietnam use IFRS?

- Vietnam does not currently require the use of full International Financial Reporting Standards (IFRS) for most companies. Instead, it uses Vietnamese Accounting Standards (VAS), which are based on older IFRS versions but with significant local adaptations. However, the Ministry of Finance has approved a roadmap for voluntary IFRS adoption starting in 2022 and mandatory adoption for certain entities expected after 2025.

What is the timeline for application of IFRS in Vietnam?

- Vietnam plans to implement International Financial Reporting Standards (IFRS) in phases starting from 2022. Voluntary adoption by selected public interest entities began in 2022, with mandatory application for certain large and listed enterprises expected from 2025 onwards as per the Ministry of Finance’s roadmap. Full nationwide application is targeted by 2030.

Which countries have adopted IFRS Standards?

- Over 140 jurisdictions worldwide have adopted International Financial Reporting Standards (IFRS) in some form, including the European Union member states, Australia, Canada, and South Korea. Some countries, like the United States, have not fully adopted IFRS but permit its use in certain circumstances.