Vietnam’s personal income tax rules for foreigners have seen sweeping changes in recent months—from higher allowances and a simplified tax schedule to expanded exemptions. This article provides an essential 2026 update to help you navigate the system.

What is Personal Income Tax?

The personal income tax is what an individual needs to pay to the Vietnamese Department of Taxation based on the amount of income earned.

Sources of income that are subject to personal income tax in Vietnam include salary and wages, capital investments, capital transfer, franchising income, inheritance, etc.

Who are considered Tax Payers in Vietnam?

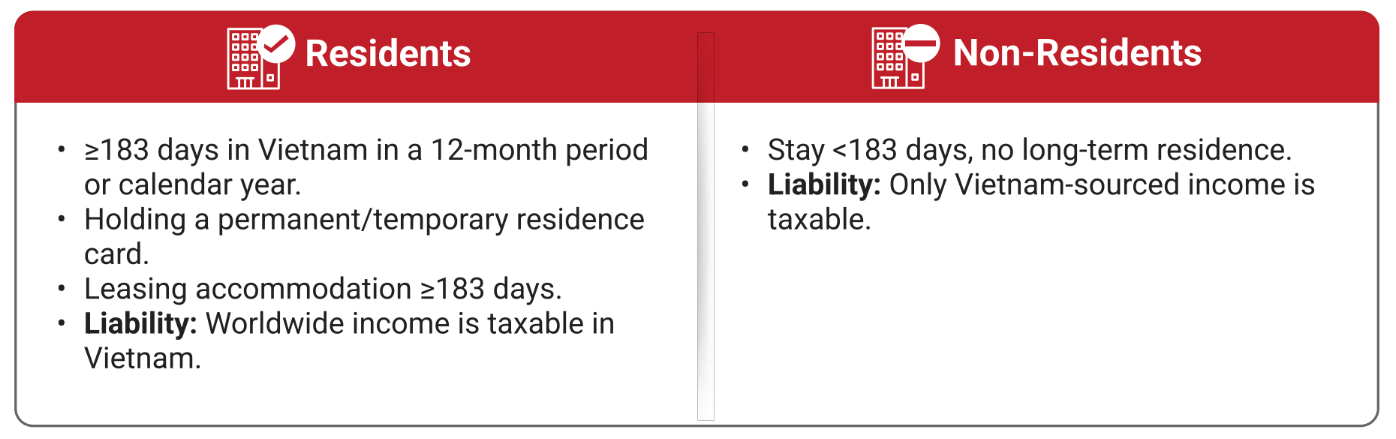

Vietnamese tax residents are taxed on worldwide income, while non-residents pay tax only on Vietnam-sourced income. You are a tax resident (subject to Vietnamese PIT on global income) if you meet any of these conditions:

- Stay in Vietnam 183 days or more in any 12-month period.

- Stay in Vietnam 183 days or more in a calendar year.

- Hold a Vietnam temporary or permanent residence card.

- Lease property in Vietnam for 183 days or more in a tax year.

If none of the above apply, you are a non-resident for PIT purposes. Non-residents (for example, someone on a short-term work contract) pay the flat 20% PIT only on Vietnam-source income. Note that Vietnam has over 80 double-taxation treaties with other countries, which may reduce or eliminate double tax on cross-border income for treaty residents.

Read More: Personal Income Tax (PIT) in Vietnam: Get A Comprehensive Visual Guide

How to Calculate an Expat’s Personal Income Tax in Vietnam

For tax residents, the monthly taxable income (salary, bonuses, allowances, etc.) is taxed at progressive rates. For non‑residents, it’s a fixed 20%.

Step 1 – Determine Your Applicable PIT Rate

For tax residents (2025 tax year): The progressive tax schedule has 7 brackets, with rates from 5% to 35%.

For tax residents (starting from 1 January 2026): The schedule is streamlined to 5 brackets, maintaining the top rate of 35% but raising the threshold for the top bracket. The new brackets are:

| Taxable income per month | Rate |

|---|---|

| Up to 10 million VND | 5% |

| Over 10 – 30 million VND | 10% |

| Over 30 – 60 million VND | 20% |

| Over 60 – 100 million VND | 30% |

| Over 100 million VND | 35% |

For non‑residents: A flat 20% of gross Vietnam‑sourced income, with no further deductions.

Step 2 – Apply Allowable Deductions

Every taxpayer receives a personal allowance that reduces taxable income. In 2025 this is 11 million VND/month. From 1 January 2026 it rises to 15.5 million VND/month.

In addition, you may claim a deduction for each qualified dependent (4.4 million VND/month in 2025, rising to 6.2 million VND/month from 2026).

Mandatory contributions to Vietnam’s social insurance (SI) and health insurance (HI) are also fully deductible. For foreign employees, SI is 8% of salary (employer pays 17.5%) and HI is 1.5% (employer pays 3%). Unemployment insurance (UI) is not required for foreigners.

Important: SI and HI contributions are capped at 20 times the base salary. The current base salary is 2,340,000 VND, so contributions apply only to salary up to 46,800,000 VND.

Step 3 – Calculate Monthly PIT

For tax residents: subtract personal allowance, dependent allowances, and insurance contributions from your gross monthly salary, then apply the progressive tax rates to the remaining amount.

For non‑residents: simply calculate 20% of each month’s Vietnam‑sourced income.

Find out more about InCorp Vietnam’s Tax Outsourcing Services for Foreign Businesses

Other Taxable Income (Non-Salary)

Many types of income besides wages are taxable at fixed rates. Important examples include:

- Business or professional income (e.g. consulting, contract work): taxed at 0.5%–5% of turnover, depending on activity. (Small-scale household businesses under VND100m per year may be exempt.)

- Non-bank interest and dividends: 5% of the income.

- Capital gains (asset transfers): 20% of the gain (for example, sale of a private company stake).

- Public share sales: 0.1% of the sales value.

- Real estate sales: 2% of the sales price (regardless of profit).

- Royalties, franchises, copyrights: 5% of the income.

- Prizes, gifts, inheritances (cash or assets): 10% of the amount (except that inheritances/gifts between close relatives are exempt, see below).

Tax residents report these incomes in their annual PIT return at the above rates. Non-residents pay the same rates on Vietnam-source non-salary income (e.g. a foreigner earning dividends from a Vietnamese company).

Tax-Free and Exempt Income

Vietnamese law exempts many income items from PIT altogether. Key tax-free incomes include:

- Family transfers: Inheritances and gifts between close relatives (spouses, parents, children, adoptees) are exempt. Likewise, transfer of a primary residence between family members (one house or land) is tax-free. Notably, transfers of real estate between direct family members incur no PIT.

- Pensions: Payments from the Vietnam Social Insurance Fund (e.g. retirement pensions) are PIT-exempt.

- Personal remittances: Money sent by relatives overseas to support a person in Vietnam is exempt.

- Scholarships and aid: Approved scholarships, foreign government aid or NGO humanitarian contributions are tax-free.

- Night/overtime bonuses: Higher-than-normal pay for night shifts or overtime is not subject to PIT.

- Insurance or compensation: Payouts from personal insurance (life, health, etc.) and certain insurance compensations are not taxable.

In practice, this means routine expat perks are often non-taxable if structured correctly. For example, Vietnam’s regulations explicitly exempt common fringe benefits for expatriates:

- Relocation allowance: A one-time payment to help an expat move to Vietnam is tax-exempt.

- Home-leave airfare: One round-trip ticket per year (to the employee’s home country) paid by the employer is non-taxable.

- Education support: Employer-paid tuition for an expat’s child (kindergarten through high school in Vietnam) is exempt.

- Lunch allowance: Employer-provided (catered) midday meals are exempt up to VND 730,000 per month.

- Uniform allowance: Cash or in-kind support for work uniforms (up to VND 5,000,000) is exempt.

- Training expenses: Fees paid by the employer for a job-related training course are exempt.

These exemptions (from various tax circulars) mean expat benefits like airfare, school fees, training, meals, etc. can often be provided tax-free if done properly.

Deduction for Charitable Donations

Donations to approved Vietnamese charities, humanitarian causes, or educational funds are deductible up to the level of your total taxable income. Keep official receipts and ensure the organization is on the government‑approved list. Unused donation deductions cannot be carried forward.

Read Related: Living in Vietnam: 10 Laws Expats Must Know

Deadline for Tax Finalizations

Vietnam uses the calendar year for PIT (1 January – 31 December). Employers withhold PIT monthly and remit it by the 20th of the next month.

At year‑end, tax finalization must be completed:

- By 31 March: Employers consolidate employees’ annual PIT and submit finalization returns for employees who authorize them.

- By 30 April (or the next working day): Individuals with multiple jobs, or who file on their own, must finalize directly. For 2025 income, the deadline was 4 May 2026.

Missing deadlines leads to fines up to 25 million VND and daily interest on unpaid tax.

Expatriates: Special Cases

- Leaving Vietnam: Foreign workers ending their contract must settle their PIT within 45 days after their exit date. You can file yourself or authorize your employer.

- Non‑resident foreigners: If you did not meet the 183‑day residency rule and have no continued income source, you are not required to file an annual PIT finalization (unless you are seeking a refund).

- Double‑tax relief: Vietnamese tax residents receive a credit for foreign taxes paid on the same income, up to the amount of Vietnamese PIT otherwise payable on that income. Always check the relevant DTA for specific rules.

- Tax codes & e‑filing: Foreign individuals receive a tax code when registering. From 2025, Vietnam is moving toward using Personal Identification Numbers (PINs), but foreign individuals (who are not issued a PIN) continue using their existing tax code. The eTax Mobile app now allows online PIT filing, pre‑populated forms, and real‑time tax status checks.

Summary

Vietnam’s PIT system for foreigners depends largely on residency:

- Tax residents pay progressive rates (5%–35%) on worldwide income

- Non‑residents pay a flat 20% on Vietnam‑sourced income

Standard deductions (personal and family allowances) significantly reduce taxable income, and many expat perks can be structured as tax‑free. Key annual deadlines are 31 March (employer finalization) and 30 April (individual finalization). With major changes taking effect from 1 January 2026, it’s essential to keep your PIT calculations and filings up to date.

Read More: Key Dates & Deadlines for Businesses in Vietnam

clients worldwide

professional staff

incorporated entities in 10 years

compliance transactions yearly

Learn the Right Setup for Business

Expansion in the Vietnam

Frequently Asked Questions

Are There Taxes In Vietnam

- Yes, Vietnam has a tax system that includes personal income tax, corporate income tax, value-added tax (VAT), and other taxes. Tax rates and regulations are governed by the Vietnamese government.

Do Vietnamese Pay Taxes

- Yes, Vietnamese citizens and businesses are required to pay taxes, including personal income tax, corporate income tax, and value-added tax, among others. The tax system is administered by the General Department of Taxation under the Ministry of Finance.

Does Vietnam Have Income Tax

- Yes, Vietnam has a personal income tax system. Residents are taxed on worldwide income, while non-residents are taxed only on Vietnam-sourced income. Tax rates vary based on income levels and residency status.

What is pit Vietnam?

- PIT in Vietnam stands for Personal Income Tax. It is the tax imposed on the income of individuals, including both Vietnamese residents and foreign individuals working or earning income in Vietnam. Residents are taxed on worldwide income, while non-residents are taxed only on Vietnam-sourced income. PIT rates in Vietnam are progressive for employment income, ranging from 5% to 35%.

What is the meaning of pit?

- In the context of Vietnam taxation, "PIT" stands for Personal Income Tax. It is a tax imposed on the income of individuals, including residents and non-residents earning income in Vietnam. Residents are taxed on their worldwide income, while non-residents are taxed only on Vietnam-sourced income. The tax rates vary depending on the type and level of income.