Vietnam’s renewable energy story is no longer just about “high potential.” As of early 2026, it is a market with real scale, real constraints, and a fast-maturing rulebook—especially after the new electricity law-and-decree package rolled out in 2024–2025. That combination is exactly what many foreign investors look for: growth strong enough to matter, and regulation clear enough to bank (even if not perfect yet).

With a population of ~101 million (2024) and continued industrial expansion, the “energy-growth” relationship remains central to Vietnam’s development model—while policy has also shifted sharply toward decarbonization and modernization.

Market forces and where the system stands now

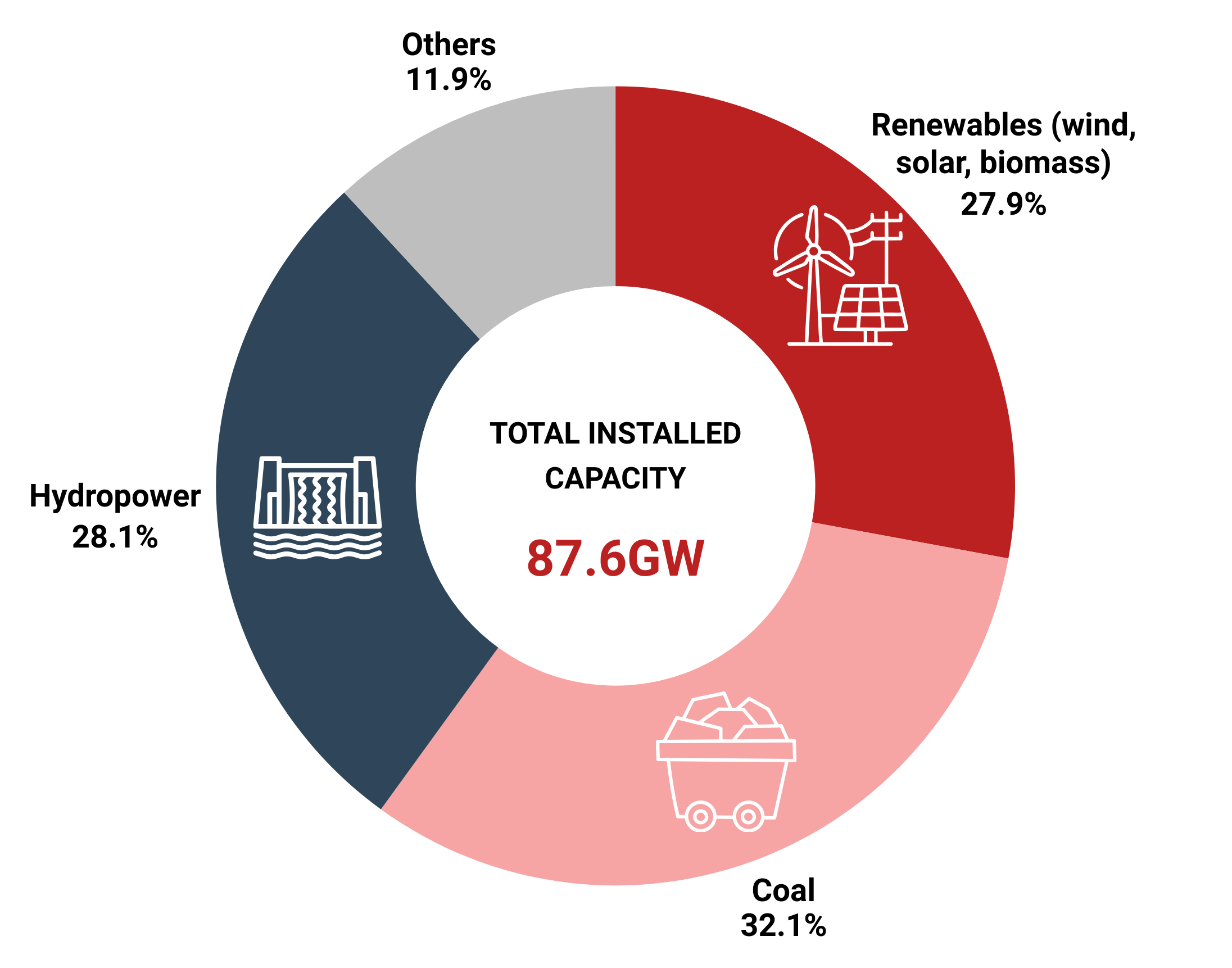

Vietnam’s national power system has reached “ASEAN scale.” By the end of 2025, total installed capacity (excluding imports) was about 87.6 GW—up roughly 6.4 GW versus 2024. In that mix, renewables (wind, solar, biomass) accounted for ~24.45 GW (27.9%), while coal was ~28.1 GW (32.1%) and hydropower ~24.64 GW (28.1%). In 2025, total electricity production and imports were estimated at ~322.8 billion kWh and peak load reached 54,370 MW (+11.1% YoY).

A major reason renewables remain investable is that they are already “in the system” at meaningful penetration—yet demand growth and regional supply constraints (notably in the North) keep the urgency high. 2025 power output was still stabilized through flexible operations and coordination, including with the National System and Market Operator.

Distributed solar is also large enough to matter. Vietnam Electricity reported that by 2025 its managed grid included 105,876 rooftop solar systems totaling ~10,220.78 MWp, with electricity fed into the grid estimated at ~10.43 billion kWh. The same report notes that additional self-consumption systems exist beyond what EVN purchases, implying the “true” rooftop footprint is larger than purchase records alone.

Grid readiness is improving—but remains the bottleneck that separates “resource potential” from “bankable megawatts.” Vietnam’s rapid solar build-out created operational stress and curtailment concerns, which lenders and developers still treat as a core risk—especially for projects in congested zones.

The growth roadmap after the revised PDP8

Vietnam’s revised power plan (approved in 2025) is designed to solve two problems at once: energy security for a fast-growing economy, and a structural shift away from coal over the long term. A Reuters summary of the plan puts total capacity by 2030 at ~183–236 GW (from “over 80 GW” in 2023), with a nationwide investment envelope cited at US$136.3 billion.

For renewable investors, the key is not only “more capacity,” but where the plan places pressure and opportunity:

- Solar is expected to command a very large share of capacity by 2030 (Reuters cites ~25.3%–31.1% of capacity).

- Onshore wind is also significant (Reuters cites ~14.2%–16.1% of capacity).

- Offshore wind is targeted at ~6–17 GW, but the timeline is effectively 2030–2035 for meaningful deployment—reflecting the reality that offshore wind is legally, financially, and technically more complex than onshore/nearshore.

It is also important to understand the “political economy” of revisions. Earlier drafts signaled that offshore wind targets would be delayed relative to earlier ambitions, and gas targets adjusted, due to project setbacks and fuel constraints—while coal, hydro, solar, and onshore wind fill near-term security needs.

This is not a reason to discount offshore wind; it is a signal to treat it as an “early-positioning” business (surveys, consents, partnerships, seabed/marine planning alignment), not just a construction business.

Ready to invest in Vietnam’s renewable energy market? InCorp Vietnam helps foreign investors structure market entry, obtain IRC/ERC licenses, and navigate regulatory approvals with confidence.

Rules that matter in practice

Between late 2024 and 2025, Vietnam introduced a tighter legal architecture for renewables and power markets—moving from a FIT-driven boom era into a more structured (and more negotiable) era.

Direct power purchase agreements

Vietnam’s DPPA framework is now anchored in Decree 57/2025/ND-CP (dated March 3, 2025), which took effect immediately and repealed Decree 80/2024. The decree covers both “private line” direct trading and “national grid” mechanisms.

Under the grid-based mechanism, eligible renewable generators include wind, solar, or biomass projects ≥10 MW that connect to the national system and participate in the competitive wholesale electricity market. Eligible large customers are connected at 22 kV or higher (including EV-charging businesses meeting the decree’s definition), and there are also “zone/cluster” retail models where authorized retail units can sign term contracts with generators.

The practical investor takeaway: DPPA is no longer hypothetical. But the commercial viability of each DPPA deal will depend on wholesale market participation mechanics, “minimum take” or qualification thresholds (which can be linked to market operation rules), and how risk is allocated through contracts.

Offshore wind and rooftop solar under Decree 58

Vietnam also issued Decree 58/2025/ND-CP detailing renewable and “new energy” development and replacing the earlier rooftop solar decree (Decree 135/2024) as of March 3, 2025.

For offshore wind, Decree 58 is highly specific and conservative in ways foreign investors must plan around:

- Preferential policies apply if the project’s investment proposal is approved before Jan 1, 2031, and (for projects selling to the national system) capacity must be within the 6,000 MW approved under planning.

- It caps marine area usage: up to 20 hectares per MW for surveys and 5 hectares per MW for implementation.

- It embeds national security governance: allocation and survey-related approvals can require written consent from multiple ministries, and transfers involving foreign investors may require additional consents.

- It explicitly ties offshore wind to a bidding/selection model, where bidding documents must respect a ceiling price not exceeding the official price bracket (see below).

For rooftop solar, Vietnam’s earlier “self-production/self-consumption” policy was launched via Decree 135/2024 (Oct 2024). It allowed broad participation (including households and industrial parks), capped typical household systems under 100 kW, and allowed selling up to 20% of installed capacity to the grid, with licensing/planning triggers for large systems (e.g., ≥1,000 kW aiming to sell to the grid).

Decree 58 then superseded Decree 135 from March 3, 2025—so current project structuring should treat Decree 58 as controlling, especially for compliance and contract terms.

Electricity operating licenses now have clearer terms

A major bankability point for foreign sponsors is licensing clarity. Under Decree 61/2025/ND-CP (implementing the Electricity Law’s licensing provisions), the term of an electricity operation license is 20 years for generation and transmission, and 10 years for distribution/wholesale/retail.

For investors, this matters directly for financing tenor alignment and for acquisition due diligence (license validity, renewal conditions, and transfer/variation requirements).

The pricing regime is now “price brackets,” not blanket FITs

Vietnam’s current approach uses official generation price brackets (ceilings) that guide negotiations rather than guaranteeing one fixed subsidized rate for all qualifying projects.

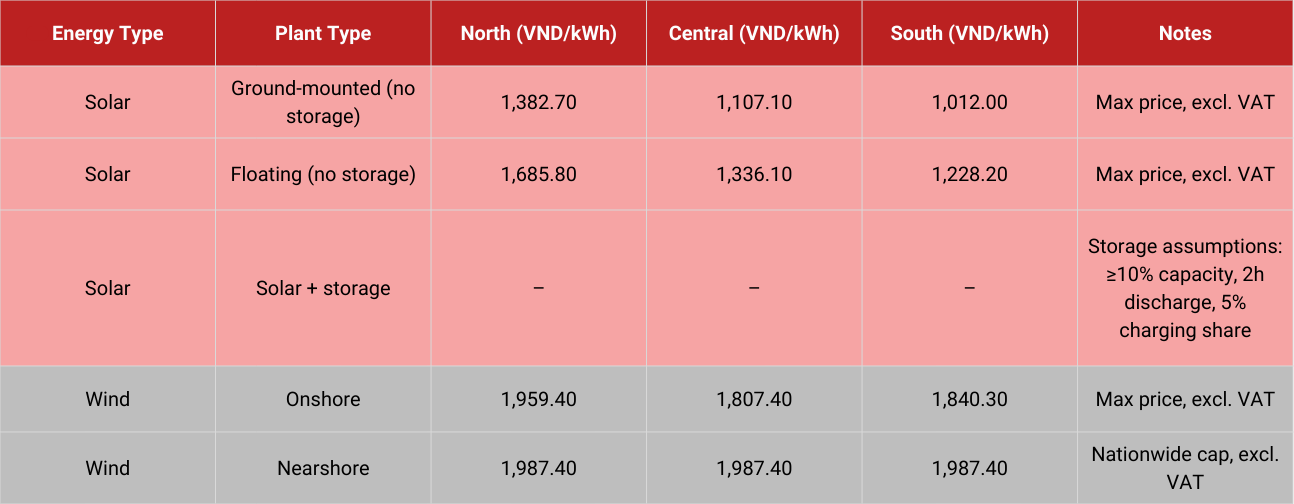

For solar in 2025, Decision 988/QD-BCT sets maximum prices (excluding VAT) by region and plant type. For example, ground-mounted solar without storage is capped at 1,382.7 VND/kWh (North), 1,107.1 (Central), 1,012.0 (South); floating solar without storage is capped at 1,685.8 / 1,336.1 / 1,228.2 VND/kWh (North/Central/South).

The same decision specifies storage parameters used in calculating the cap for solar-plus-storage: minimum storage capacity 10% of plant capacity, 2-hour storage/discharge time, and charging energy share of 5% of solar output.

For wind in 2025, Decision 1508/QD-BCT caps onshore wind at 1,959.4 VND/kWh (North), 1,807.4 (Central), 1,840.3 (South); nearshore wind is capped at 1,987.4 VND/kWh nationwide (excluding VAT).

For commercial investors, this has two implications: (1) pricing is more market-linked and negotiation-driven; (2) project competitiveness (resource quality, grid position, capex discipline, ability to add value through storage) becomes the main determinant of returns.

Investment opportunities by segment

Vietnam’s opportunity set is broader than “build a wind farm.” The most actionable paths tend to fall into a few segments with distinct risk profiles.

Utility-scale solar and wind remain investable, but the winning strategy has shifted from “race to COD for FIT” to “win on fundamentals.” Under price brackets, bankability tends to favor (a) strong resource regions, (b) grid-access realism, and (c) sponsors who can manage curtailment and dispatch risk through design choices (including storage where economics work) and conservative underwriting.

Corporate offtake is becoming the commercial bridge between investor appetite and Vietnam’s grid constraints. DPPA under Decree 57 creates a legal path for large power users to buy from renewable generators either through private lines or via the grid-based mechanism—opening a route for “green power” sourcing without depending solely on traditional PPA pathways.

Rooftop solar and C&I solutions (often bundled with energy management) can be compelling where the customer’s load profile supports self-consumption economics. However, investors must structure projects tightly around the “self-consumption first” principle and the rules governing surplus sales to the grid (and related licensing/planning triggers).

Legacy “transitional” projects are still working through commercialization and pricing. As of May 23, 2024, 81/85 transitional renewable projects (~4,597.86 MW) had submitted pricing negotiation documents, and 29 plants/plant-parts (~1,577.65 MW) had completed COD procedures and generated commercial power, producing over 2.597 billion kWh cumulatively from COD to that date.

For secondary-market investors, these assets can be attractive—but only with disciplined diligence on tariff status, payment mechanics, compliance, and dispute history.

Finally, offshore wind is a “position now, build later” market. Decree 58 provides more predictability on incentives, area use, surveys, bidder selection, and the role of state and security institutions—but it also formalizes multi-ministry consent requirements and complex eligibility rules. That means early-stage success often looks like: securing survey rights, building a credible consortium (technical + financial + local alignment), and designing a development roadmap that can survive a multi-year approval timeline.

Entering Vietnam’s energy market requires more than capital. It requires the right structure.

InCorp Vietnam helps foreign investors establish compliant platforms for investment, licensing, and long-term operations.

A practical entry playbook for foreign investors

A workable market-entry model in Vietnam usually starts with choosing the right “vehicle” and approvals path—then building a development pipeline that matches Vietnam’s planning and licensing logic.

Most foreign investors entering by establishing an operating company will navigate the “IRC → ERC” structure: obtain an Investment Registration Certificate (IRC) for the project, then an Enterprise Registration Certificate (ERC) for the legal entity. A commonly cited planning assumption for licensing is ~30–45 working days, but timelines vary depending on project complexity, location, and sector-specific approvals.

From a practical execution standpoint, investors tend to succeed when they treat Vietnam as a sequenced approvals market:

First, align the project with planning and location logic. In Vietnam, land and power planning integration is not a back-office detail; it is what determines whether later licenses and grid connection are feasible. This is even more important after the Land Law’s earlier entry into force (moved forward to Aug 1, 2024), which accelerated a wave of new implementing guidance for land procedures and valuation.

Second, structure the revenue model around the correct regime: traditional PPA, DPPA (private line or grid-based), rooftop self-consumption (with limited surplus sales), or offshore wind bidding. Misclassifying the model early often leads to delays later.

Third, plan licensing and compliance around the actual operating activity. Generation and transmission licenses can run up to 20 years, while distribution/retail activities typically run 10 years, so financing and shareholder agreements should match the regulatory tenor.

Fourth, run “Vietnam-style” diligence. Beyond technical feasibility, foreign investors should stress-test: (a) grid connection risk and curtailment history, (b) tariff and payment track record, (c) land status and compensation/resettlement exposure, and (d) any security-related consent requirements (especially for offshore wind).

For teams that want a faster and lower-risk start, a common commercial path is to enter via acquisition or partnership with operating assets (or late-stage projects) while building a greenfield pipeline in parallel—so that early cash flows support long-cycle development.

Risks and how to de-risk

Vietnam’s renewable market is attractive precisely because it is transitioning from a subsidy-led surge to a rules-and-market era. That transition creates opportunity—but also headline risks that investors must price correctly.

The most visible risk in 2025 was policy and payment uncertainty for some legacy FIT-era projects. Reuters reported investor petitions warning that retroactive changes and unilateral payment adjustments could jeopardize billions of dollars of renewable investments and create loan-default risks, including cases where EVN subsidiaries were described as applying provisional tariffs and withholding payments.

If you are buying operating assets, this is the diligence question: “What is the project’s tariff entitlement and compliance status, and what is the realistic payment pathway in the current environment?”

Foreign investor sentiment has also been affected by project delays and regulatory friction. Reuters reported that Enel prepared to exit Vietnam amid delays and infrastructure challenges, following other withdrawals by Equinor and Orsted.

The lesson is not “don’t invest.” It is that Vietnam rewards investors who can execute through administrative complexity, localize development capacity, and structure projects around the current (not historical) pricing and contracting rules.

Curtailment remains a structural risk, especially for solar-heavy regions and for projects built ahead of grid reinforcement. Industry commentary has flagged curtailment as a bankability issue for years; it still matters in 2026.

Mitigation typically comes from a combination of site selection, realistic grid studies, conservative base-case dispatch assumptions, contractual risk allocation, and (where feasible) storage or demand-shaping solutions.

Finally, regulatory sophistication is rising—especially around offshore wind governance. Decree 58 formalizes multi-ministry consents, marine area constraints, and rules for investor selection and ceiling prices in bidding documents. Investors should treat compliance and stakeholder alignment as a core workstream from day one, not something to “solve later.”

Vietnam’s carbon policy direction also matters commercially. The pilot launch of an emissions trading scheme (ETS) for major emitting sectors (including thermal power, cement, and steel) is intended to cover a large share of national emissions over time and can increase corporate demand for clean power and carbon-efficient operations.

The practical conclusion is straightforward: Vietnam is still one of Southeast Asia’s most scalable renewable markets, but “winning” now means building investability—through legal structuring, planning alignment, bankable contracting, and risk-managed execution—rather than relying on one-size-fits-all incentives.

If the goal is to enter quickly and credibly—especially for foreign sponsors that need a compliant local platform for investment, hiring, contracting, and licensing—working with an incorporation-and-licensing specialist such as InCorp Vietnam (or equivalent local advisers) can reduce timeline risk and improve diligence quality before capital is committed.

clients worldwide

professional staff

incorporated entities in 10 years

compliance transactions yearly

Learn the Right Setup for Business

Expansion in the Vietnam

Frequently Asked Questions

What are the 7 main sources of renewable energy?

- The 7 main sources of renewable energy are solar energy, wind energy, hydro (water) energy, tidal energy, geothermal energy, biomass energy, and wave energy. These sources are naturally replenished and help reduce reliance on fossil fuels while lowering greenhouse gas emissions.